Residential PV Systems

Representative Technology

For the ATB, residential PV systems are modeled for a 5.0-kWDC fixed tilt (25°), roof-mounted system. Flat-plate PV can take advantage of direct and indirect insolation, so PV modules need not directly face and track incident radiation. This gives PV systems a broad geographical application, especially for residential PV systems.

Resource Potential

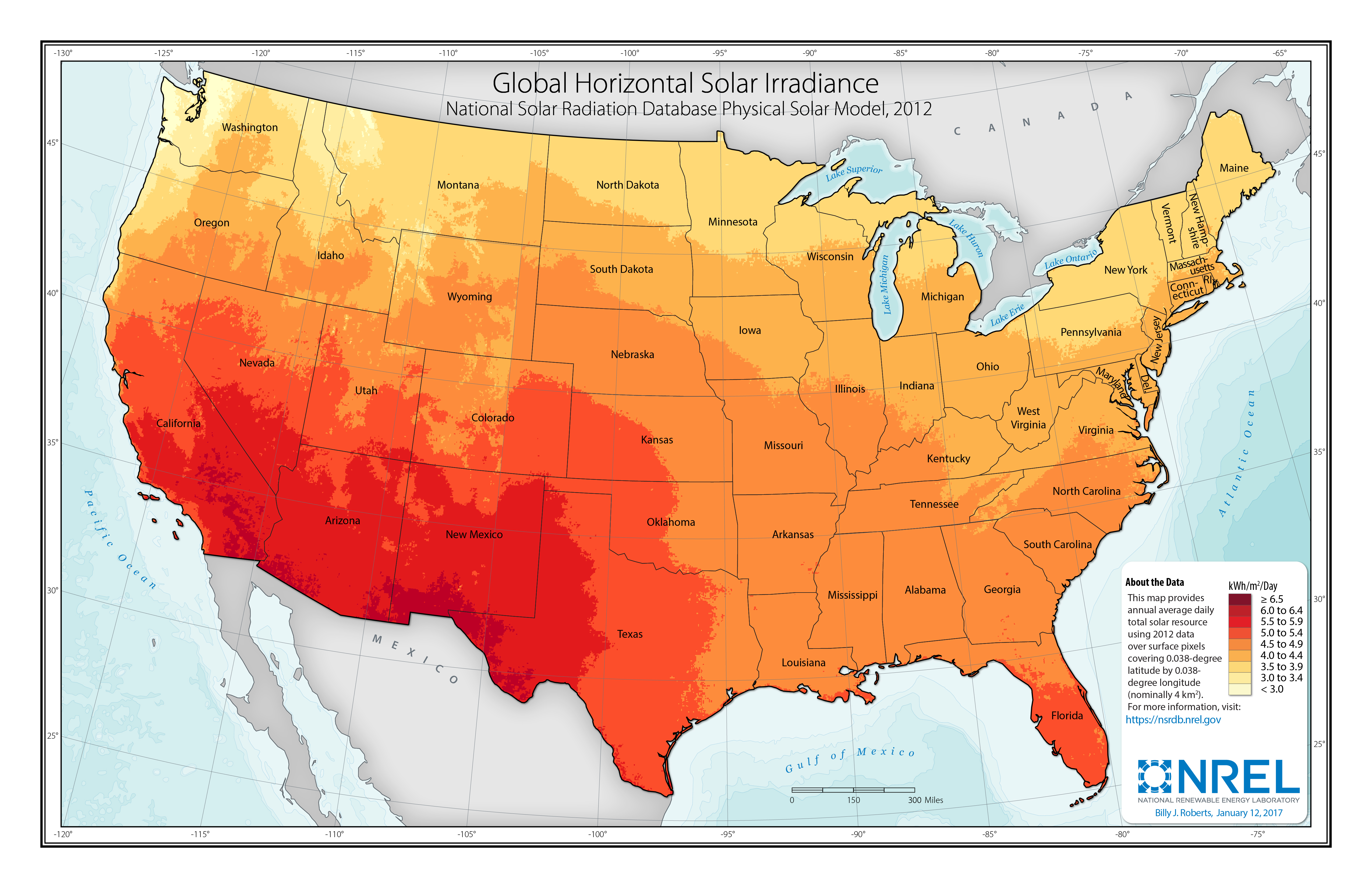

Solar resources across the United States are mostly good to excellent at about 1,000-2,500 kWh/m2/year. The Southwest is at the top of this range, while only Alaska and part of Washington are at the low end. The range for the contiguous United States is about 1,350-2,500 kWh/m2/year. Nationwide, solar resource levels vary by about a factor of two.

Distributed-scale PV is assumed to be configured as a fixed-tilt, roof-mounted system. Compared to utility-scale PV, this reduces both the potential capacity factor and amount of land (roof space) that is available for development. A recent study of rooftop PV technical potential (Gagnon et al. 2016) estimated that as much as 731 GW (926 TWh/yr) of potential exists for small buildings (< 5,000 m2) and 386 GW (506 TWh/yr) of potential exists for medium (5,000-25,000 m2) and large buildings (> 25,000 m2).

Renewable energy technical potential, as defined by Lopez et al. (2012), represents the achievable energy generation of a particular technology given system performance, topographic limitations, and environmental and land-use constraints. The primary benefit of assessing technical potential is that it establishes an upper-boundary estimate of development potential. It is important to understand that there are multiple types of potential-resource, technical, economic, and market (see NREL: "Renewable Energy Technical Potential").

Base Year and Future Year Projections Overview

The Base Year estimates rely on modeled CAPEX and O&M estimates benchmarked with industry and historical data. Capacity factor is estimated based on hours of sunlight at latitude for five representative geographic locations in the United States.

Future year projections are derived from analysis of published projections of PV CAPEX and bottom-up engineering analysis of O&M costs. Three different technology cost scenarios were developed for scenario modeling as bounding levels:

- Constant Technology Cost Scenario: no change in CAPEX, O&M, or capacity factor from 2017 to 2050; consistent across all renewable energy technologies in the ATB

- Mid Technology Cost Scenario: based on the median of literature projections of future CAPEX; O&M technology pathway analysis

- Low Technology Cost Scenario: based on the low bound of literature projections of future CAPEX and O&M technology pathway analysis.

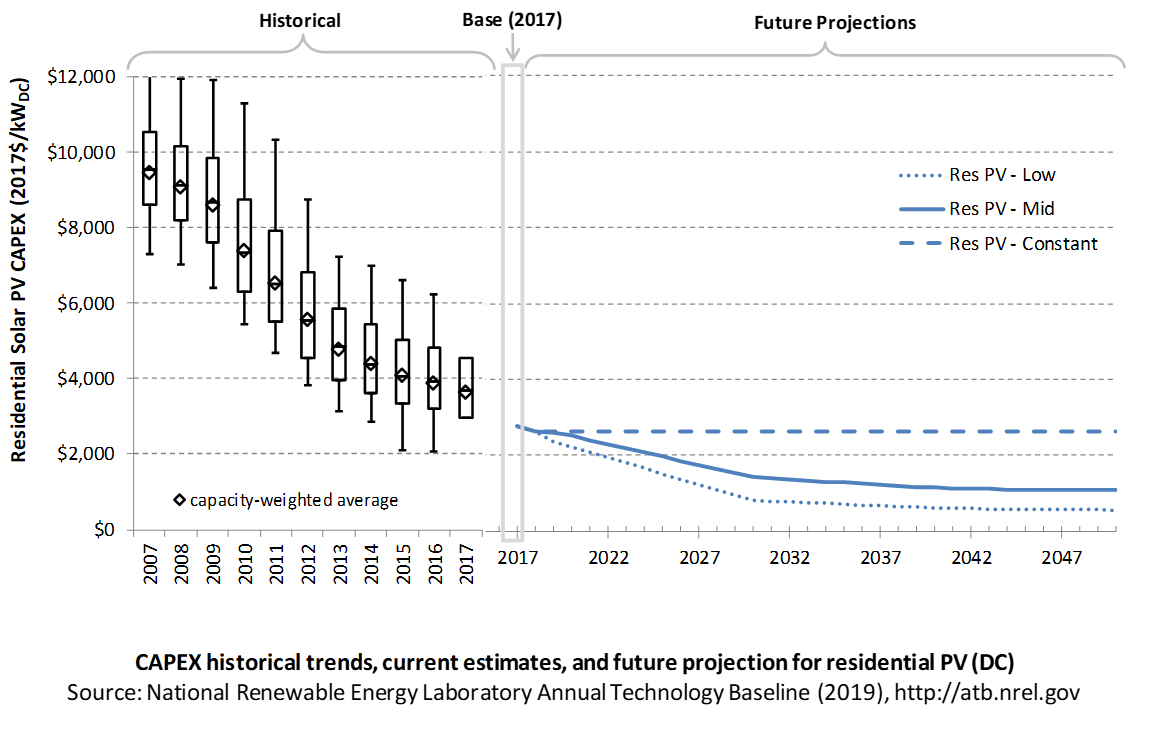

Capital Expenditures (CAPEX): Historical Trends, Current Estimates, and Future Projections

Capital expenditures (CAPEX) are expenditures required to achieve commercial operation in a given year. These expenditures include the hardware, the balance of system (e.g., site preparation, installation, and electrical infrastructure), and financial costs (e.g., development costs, onsite electrical equipment, and interest during construction) and are detailed in CAPEX Definition. In the ATB, CAPEX reflects typical plants and does not include differences in regional costs associated with labor, materials, taxes, or system requirements. The related Standard Scenarios product uses Regional CAPEX Adjustments. The range of CAPEX demonstrates variation with resource in the contiguous United States.

The following figure shows the Base Year estimate and future year projections for CAPEX costs. Three cost scenarios are represented: Constant, Mid, and Low technology cost. Historical data from residential PV installed in the United States are shown for comparison to the ATB Base Year estimates. The estimate for a given year represents CAPEX of a new plant that reaches commercial operation in that year.

Recent Trends

Reported residential PV installation CAPEX (Barbose and Dargouth 2018) is shown in box-and-whiskers format for comparison to historical residential PV benchmark overnight capital cost (Fu, Feldman, and Margolis 2018) and the ATB estimates of future CAPEX projections. The data in Barbose and Dargouth (2018) represent 81% of all U.S. residential and commercial PV capacity installed through 2016 and 75% of capacity installed in 2017.

The difference in each year's price between the market and benchmark data reflects differences in methodologies. There are a variety of reasons reported and benchmark prices can differ, as enumerated by Barbose and Dargouth (2018) and Bolinger and Seel (2018), including:

- Timing-related issues: For instance, the time between contract completion date and project placed in service may vary.

- Variations over time in the size, technology, installer margin, and design of systems installed in a given year

- Which cost categories are included in CAPEX (e.g., financing costs and initial O&M expenses).

Due to the investment tax credit, projects are encouraged to include as many costs incurred in the upfront CAPEX to receive a higher tax credit, which may have otherwise been reported as operating costs. The bottom-up benchmarks are more reflective of an overnight capital cost, which is in line with the ATB methodology of inputting overnight capital cost and calculating construction financing to derive CAPEX.

PV pricing and capacities are quoted in kWDC (i.e., module rated capacity) unlike other generation technologies, which are quoted in kWAC. For PV, this would correspond to the combined rated capacity of all inverters. This is done because kWDC is the unit that the majority of the PV industry uses. Although costs are reported in kWDC, the total CAPEX includes the cost of the inverter, which has a capacity measured in kWAC.

CAPEX estimates for 2018 reflect a continued rapid decline in pricing supported by analysis of recent system cost and pricing for projects that became operational in 2018 (Feldman and Margolis 2018).

Base Year Estimates

For illustration in the ATB, a representative residential-scale PV installation is shown. Although the PV technologies vary, typical installation costs are represented with a single estimate because the CAPEX does not vary with solar resource.

Although the technology market share may shift over time with new developments, the typical installation cost is represented with the projections above.

A system price of $2.77/WDC in 2017 and $2.64/WDC in 2018 are based on bottom-up benchmark analysis reported in U.S. Solar Photovoltaic System Cost Benchmark Q1 2018 (adjusted for inflation) (Fu, Feldman, and Margolis 2018). These figures are in line with other estimated system prices reported in Q2/Q3 2018 Solar Industry Update (Feldman and Margolis 2018).

The Base Year CAPEX estimates should tend toward the low end of observed cost because no regional impacts are included. These effects are represented in the historical market data.

Future Year Projections

Projections of future residential PV installation CAPEX are based on seven system price projections from six separate institutions made in the last two years. We adjusted the "min," "median," and "max" projections in a few different ways. All 2017 and 2018 pricing are based on the bottom-up benchmark analysis reported in U.S. Solar Photovoltaic System Cost Benchmark Q1 2018 (adjusted for inflation) (Fu, Feldman, and Margolis 2018). These figures are in line with other estimated system prices reported in Q2/Q3 2018 Solar Industry Update (Feldman and Margolis 2018).

We adjusted the Mid and Low cost projections for 2019-2050 to remove distortions caused by the combination of forecasts with different time horizons and based on internal judgment of price trends. The Constant technology cost scenario is kept constant at the 2018 CAPEX value, assuming no improvements beyond 2018.

A detailed description of the methodology for developing future year projections is found in Projections Methodology.

Technology innovations that could impact future O&M costs are summarized in LCOE Projections.

CAPEX Definition

Capital expenditures (CAPEX) are expenditures required to achieve commercial operation in a given year. For residential PV, this is modeled for a host-owned business model only.

For the ATB, and based on EIA (2016b) and the NREL Solar-PV Cost Model (Fu, Feldman, and Margolis 2018), the distributed residential solar PV plant envelope is defined to include:

- Hardware

- Module supply

- Power electronics, including inverters

- Racking

- Foundation

- AC and DC wiring materials and installation

- Balance of system (BOS)

- Site and/or roof preparation

- Permitting, inspection, and interconnection costs

- Project indirect costs, including costs related to engineering, distributable labor and materials, construction management start up and commissioning, and contractor overhead costs, fees, and profit

- Financial costs

- Owners costs, such as development costs, legal fees, insurance costs.

CAPEX can be determined for a plant in a specific geographic location as follows:

Regional cost variations are not included in the ATB (CapRegMult = 1). Because distributed PV plants are located directly at the end use, there are no grid connection costs (GCC = 0). In the ATB, the input value is overnight capital cost (OCC) and details to calculate interest during construction (ConFinFactor).

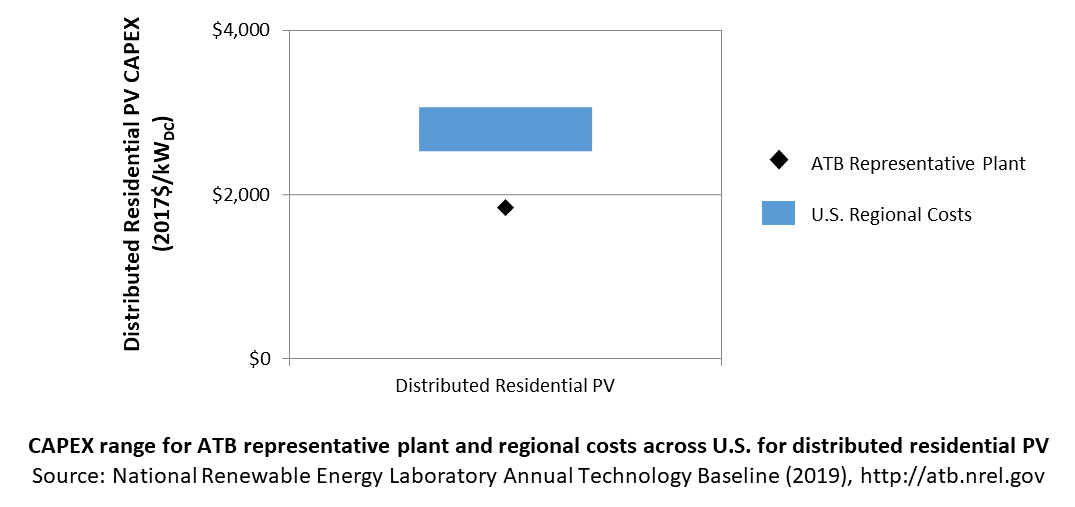

In the ATB, CAPEX represents a typical distributed residential/commercial PV plant and does not vary with resource. Regional cost effects associated with labor rates, material costs, and other regional effects as defined by EIA (2016b) expand the range of CAPEX. Unique land-based spur line costs based on distance and transmission line costs are not estimated. The following figure illustrates the ATB representative plant relative to the range of CAPEX including regional costs across the contiguous United States. The ATB representative plants are associated with a regional multiplier of 1.0.

Standard Scenarios Model Results

ATB CAPEX, O&M, and capacity factor assumptions for the Base Year and future projections through 2050 for Constant, Mid, and Low technology cost scenarios are used to develop the NREL Standard Scenarios using the ReEDS model. See ATB and Standard Scenarios.

CAPEX in the ATB does not represent regional variants (CapRegMult) associated with labor rates, material costs, etc., but dSolar does include 134 regional multipliers (EIA 2016b).

Operation and Maintenance (O&M) Costs

Operations and maintenance (O&M) costs represent the annual expenditures required to operate and maintain a solar PV plant over its lifetime, including:

- Insurance, property taxes, site security, legal and administrative fees, and other fixed costs

- Present value and annualized large component replacement costs over technical life (e.g., inverters at 15 years)

- Scheduled and unscheduled maintenance of solar PV plants, transformers, etc. over the technical lifetime of the plant (e.g., general maintenance, including cleaning and vegetation removal).

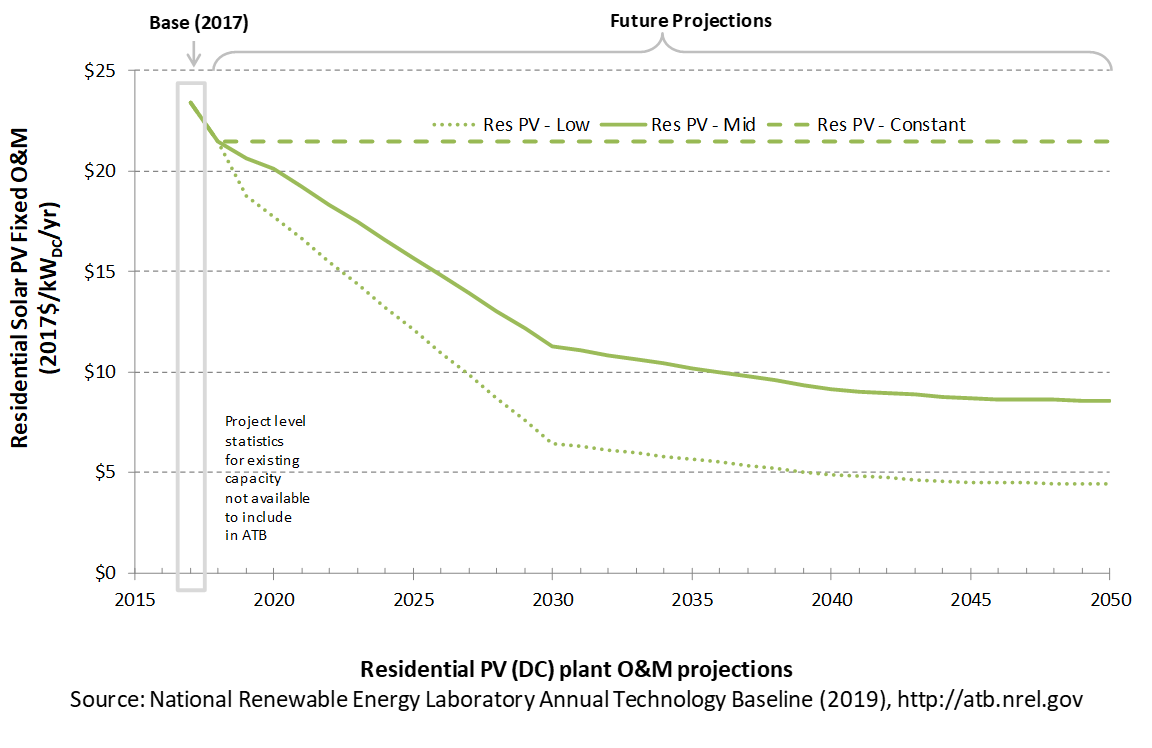

The following figure shows the Base Year estimate and future year projections for fixed O&M (FOM) costs. Three cost scenarios are represented. The estimate for a given year represents annual average FOM costs expected over the technical lifetime of a new plant that reaches commercial operation in that year.

Base Year Estimates

FOM of $23/kWDC - yr based on modeled pricing for a commercial PV system quoted in Q1 2017 as reported by Fu, Feldman, and Margolis (2018), adjusted for inflation. The values in this report (ATB 2019) are higher than those from ATB 2018 to better align with the benchmarks reported in Fu, Feldman, and Margolis (2018); the previous edition relied solely on an O&M-to-CAPEX ratio, derived from multiple reports. A wide range in reported prices exists in the market, and in part, it depends on what maintenance practices exist for a particular system. These cost categories include asset management (including compliance and reporting for incentive payments), different insurance products, site security, cleaning, vegetation removal, and failure of components. Not all these practices are performed for each system; additionally, some factors depend on the quality of the parts and construction. NREL analysts estimate O&M costs can range from $0 to $40/kWDC - yr.

Future Year Projections

FOM for 2018 is also based on pricing reported in Fu, Feldman, and Margolis (2018), adjusted for inflation. From 2019-2050, FOM is based on the historical average ratio of O&M costs ($/kW-yr) to CAPEX costs ($/kW), 0.8:100, as reported by Fu, Feldman, and Margolis (2018). Historically reported data suggest O&M and CAPEX cost reductions are correlated; from 2010 to 2018 benchmark residential PV O&M and CAPEX costs fell 60% and 63% respectively, as reported by Fu, Feldman, and Margolis (2018).

A detailed description of the methodology for developing future year projections is found in Projections Methodology.

Technology innovations that could impact future O&M costs are summarized in LCOE Projections.

Capacity Factor: Expected Annual Average Energy Production Over Lifetime

The capacity factor represents the expected annual average energy production divided by the annual energy production, assuming the plant operates at rated capacity for every hour of the year. It is intended to represent a long-term average over the lifetime of the plant. It does not represent interannual variation in energy production. Future year estimates represent the estimated annual average capacity factor over the technical lifetime of a new plant installed in a given year.

PV system capacity is not directly comparable to other technologies' capacity factors. Other technologies' capacity factors are represented in exclusively AC units (see Solar PV AC-DC Translation). However, because PV pricing in this ATB documentation is represented in $/WDC, PV system capacity is a DC rating. Because each technology uses consistent capacity ratings, the LCOEs are comparable.

The capacity factor is influenced by the hourly solar profile, technology (e.g., thin-film versus crystalline silicon), axis type (e.g., none, one, or two), expected downtime, and inverter losses to transform from DC to AC power. The DC-to-AC ratio is a design choice that influences the capacity factor. PV plant capacity factor incorporates an assumed degradation rate of 0.75%/year (Fu, Feldman, and Margolis 2018) in the annual average calculation. R&D could lower degradation rates of PV plant capacity factor; future projections for Mid and Low cost scenarios reduce degradation rates by 2050, using a straight-line basis, to 0.5%/year and 0.2%/year respectively.

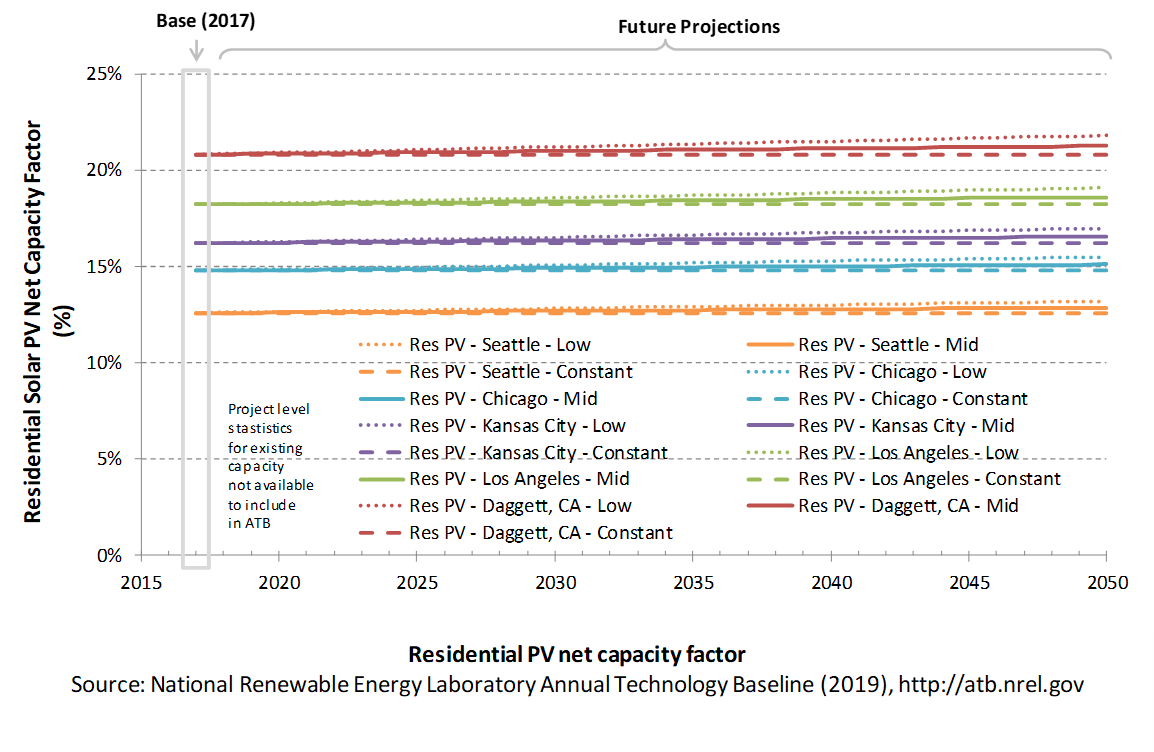

The following figure shows a range of capacity factors based on variation in solar resource in the contiguous United States. The range of the Base Year estimates illustrate the effect of locating a utility-scale PV plant in places with lower or higher solar irradiance. These five values use specific locations as examples of high (Daggett, CA), high-mid (Los Angeles, CA), mid (Kansas City, MO), low-mid (Chicago, IL), and low (Seattle, WA) resource areas in the United States as implemented in the System Advisor Model using PV system characteristics from Fu, Feldman, and Margolis (2018).

Base Year Estimates

For illustration in the ATB, a range of capacity factors is associated with the range of solar irradiance for three resource locations in the contiguous United States:

- Low: Seattle, Washington

- Low-mid: Chicago, Illinois

- Mid: Kansas City, Missouri

- High-mid: Los Angeles, California

- High: Daggett, California

First-year operation capacity factors as modeled range from 13.4% to 22.2%, though these depend significantly on geography and system configuration (e.g., fixed-tilt versus single-axis tracking).

Over time, PV installation output is reduced due to degradation in module quality. This degradation is accounted in ATB estimates of capacity factor over the 30-year lifetime of the plant. The adjusted average capacity factor values in the ATB Base Year are 12.6%, 14.8%, 16.2%, 18.2%, and 20.8%.

Future Year Projections

Projections of capacity factors for plants installed in future years are unchanged from the Base Year for the Constant technology cost scenario. Capacity factors for Mid and Low cost scenarios are projected to increase over time, caused by a straight-line reduction in PV plant capacity degradation rates, reaching 0.5%/year and 0.2%/year by 2050 for the Mid and Low cost scenarios respectively. The following table summarizes the difference in average capacity factor in 2050 caused by different degradation rates in the Constant, Mid, and Low cost scenarios.

| Seattle, WA | Chicago, IL | Kansas City, MO | Los Angeles, CA | Daggett, CA | |

| Low Cost (0.30% degradation rate) | 13.1% | 15.4% | 16.8% | 18.9% | 21.6%< |

| Mid Cost (0.50% degradation rate) | 12.9% | 15.1% | 16.6% | 18.6% | 21.3% |

| Constant Cost (0.75% degradation rate) | 12.6% | 14.8% | 16.2% | 18.2% | 20.8% |

Solar PV plants have very little downtime, inverter efficiency is already optimized, and tracking is already assumed. That said, there is potential for future increases in capacity factors through technological improvements beyond lower degradation rates, such as less panel reflectivity and improved performance in low-light conditions.

Standard Scenarios Model Results

ATB CAPEX, O&M, and capacity factor assumptions for the Base Year and future projections through 2050 for Constant, Mid, and Low technology cost scenarios are used to develop the NREL Standard Scenarios using the ReEDS model. See ATB and Standard Scenarios.

dSolar does not endogenously consider curtailment from surplus renewable energy generation, though this is a feature of the linked ReEDS-dSolar model (Cole et al. 2016), where balancing area-level marginal curtailments can be applied to distributed PV generation as determined by scenario constraints.

Plant Cost and Performance Projections Methodology

Currently, CAPEX – not LCOE – is the most common metric for PV cost. Due to differing assumptions in long-term incentives, system location and production characteristics, and cost of capital, LCOE can be confusing and often incomparable between differing estimates. While CAPEX also has many assumptions and interpretations, it involves fewer variables to manage. Therefore, PV projections in the ATB are driven entirely by plant and operational cost improvements.

We created Constant, Mid, and Low technology cost CAPEX cases to explore the range of possible outcomes of future PV cost improvements. The Constant technology case represents no CAPEX improvements made beyond today, the Mid case represents current expectations of price reductions in a "business-as-usual" scenario, and the Low case represents current expectations of potential cost reductions given improved R&D funding and more aggressive global deployment targets.

While CAPEX is one of the drivers to lower costs, R&D efforts continue to focus on other areas to lower the cost of energy from residential PV. While these are not incorporated in the ATB, they include longer system lifetime, improved performance and reliability, and lower cost of capital.

Projections of future residential PV installation CAPEX are based on seven system price projections from six separate institutions. Projections include short-term U.S. price forecasts and long-term global and U.S. price forecasts made in the past two years. The short-term forecasts were primarily provided by market analysis firms with expertise in the PV industry, through a subscription service with NREL. The long-term forecasts primarily represent the collection of publicly available, unique forecasts with either a long-term perspective of solar trends or through capacity expansion models with assumed learning by doing.

- Short-Term Forecast Institutions: Bloomberg New Energy Finance, CAISO, GTM Research, Navigant Research (Labastida and Gauntlett 2016), U.S. Energy Information Administration

- Long-Term Forecast Institutions: Bloomberg New Energy Finance, International Energy Agency.

In instances in which literature projections did not include all years, a straight-line change in price was assumed between any two projected values. To generate Mid and Low technology cost scenarios we took the "median" and "min" of the data sets; however, we only included short-term U.S. forecasts until 2030 as they focus on near-term pricing trends within the industry. Starting in 2030, we include long-term global and U.S. forecasts in the data set, as they focus more on long-term trends within the industry. It is also assumed after 2025 U.S. prices will be on par with global averages. Many of the global projections are weighted heavily toward western countries (e.g., European countries, Japan, and the United States), and in the long-term, the United States should follow global trends. The federal tax credit for solar assets reverts down to 10% for all projects placed in service after 2023, which has the potential to lower upfront financing costs and remove any distortions in reported pricing, compared to other global markets. Additionally, a larger portion of the United States will have a more mature PV market, which should result in a narrower price range. Many institutions used one system price for all countries. Changes in price for the Mid and Low technology cost scenarios between 2020 and 2030 are interpolated on a straight-line basis.

We adjusted the "median" and "min" projections in a few different ways. All 2017 and 2018 pricing are based on the bottom-up benchmark analysis reported in U.S. Solar Photovoltaic System Cost Benchmark Q1 2018 (adjusted for inflation) (Fu, Feldman, and Margolis 2018). These figures are in line with other estimated system prices reported in Q2/Q3 2018 Solar Industry Update (Feldman and Margolis 2018).

We adjusted the Mid and Low cost projections for 2019-2050 to remove distortions caused by the combination of forecasts with different time horizons and based on internal judgment of price trends. The Constant technology cost scenario is kept constant at the 2018 CAPEX value, assuming no improvements beyond 2018.

From 2019-2050, FOM is based on the historical average ratio of O&M costs ($/kW-yr) to CAPEX costs ($/kW), 0.8:100, as reported by Fu, Feldman, and Margolis (2018). Historically reported data suggest O&M and CAPEX cost reductions are correlated; from 2010 to 2018 benchmark residential PV O&M and CAPEX costs fell 60% and 63% respectively, as reported by Fu, Feldman, and Margolis (2018).

Projections of capacity factors for plants installed in future years are unchanged from 2018 for the Constant technology cost scenario. Capacity factors for Mid and Low cost scenarios are projected to increase over time, caused by a straight-line reduction in PV plant capacity degradation rates from 0.75%, reaching 0.5%/year and 0.2%/year by 2050 for the Mid and Low cost scenarios, respectively.

Levelized Cost of Energy (LCOE) Projections

Levelized cost of energy (LCOE) is a summary metric that combines the primary technology cost and performance parameters: CAPEX, O&M, and capacity factor. It is included in the ATB for illustrative purposes. The ATB focuses on defining the primary cost and performance parameters for use in electric sector modeling or other analysis where more sophisticated comparisons among technologies are made. The LCOE accounts for the energy component of electric system planning and operation. The LCOE uses an annual average capacity factor when spreading costs over the anticipated energy generation. This annual capacity factor ignores specific operating behavior such as ramping, start-up, and shutdown that could be relevant for more detailed evaluations of generator cost and value. Electricity generation technologies have different capabilities to provide such services. For example, wind and PV are primarily energy service providers, while the other electricity generation technologies provide capacity and flexibility services in addition to energy. These capacity and flexibility services are difficult to value and depend strongly on the system in which a new generation plant is introduced. These services are represented in electric sector models such as the ReEDS model and corresponding analysis results such as the Standard Scenarios.

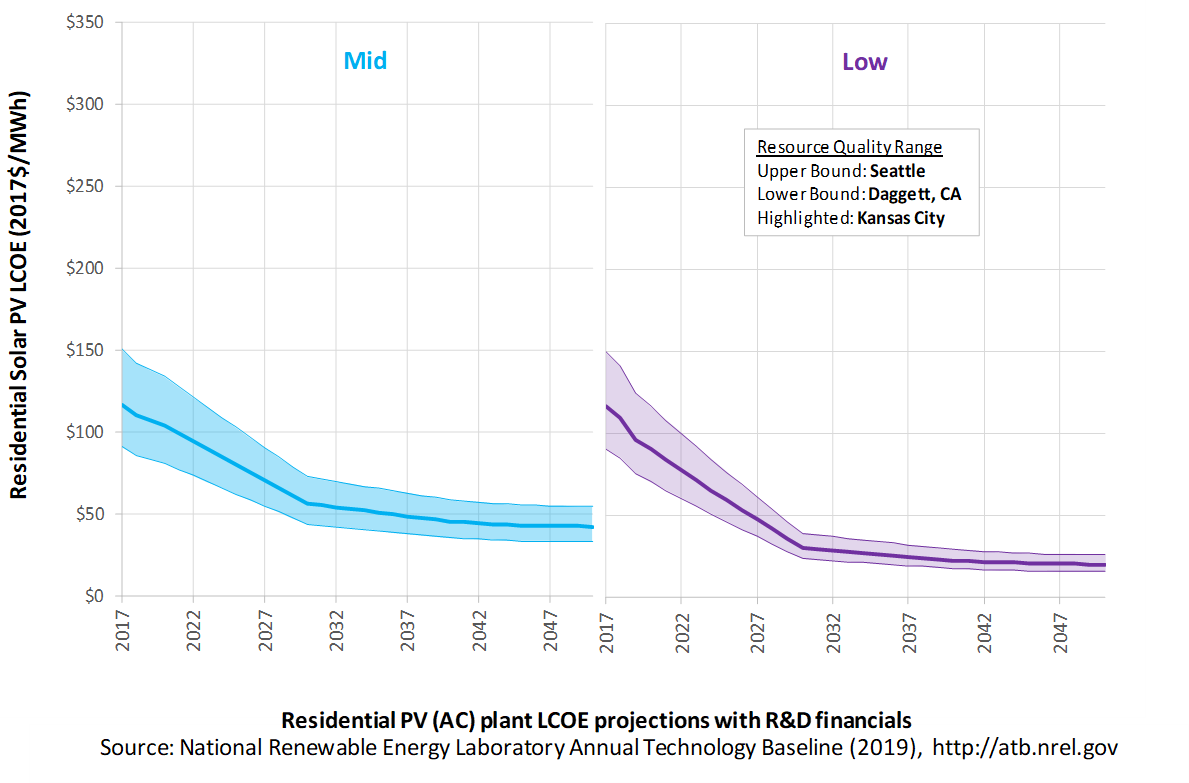

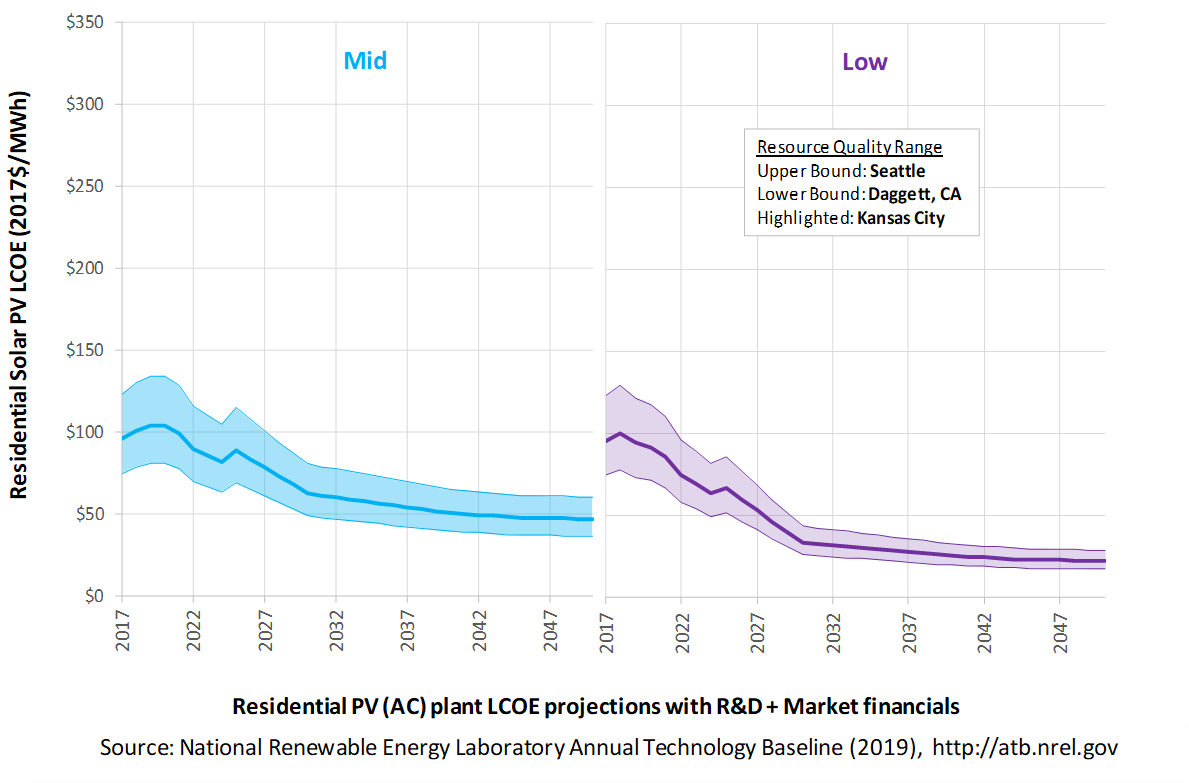

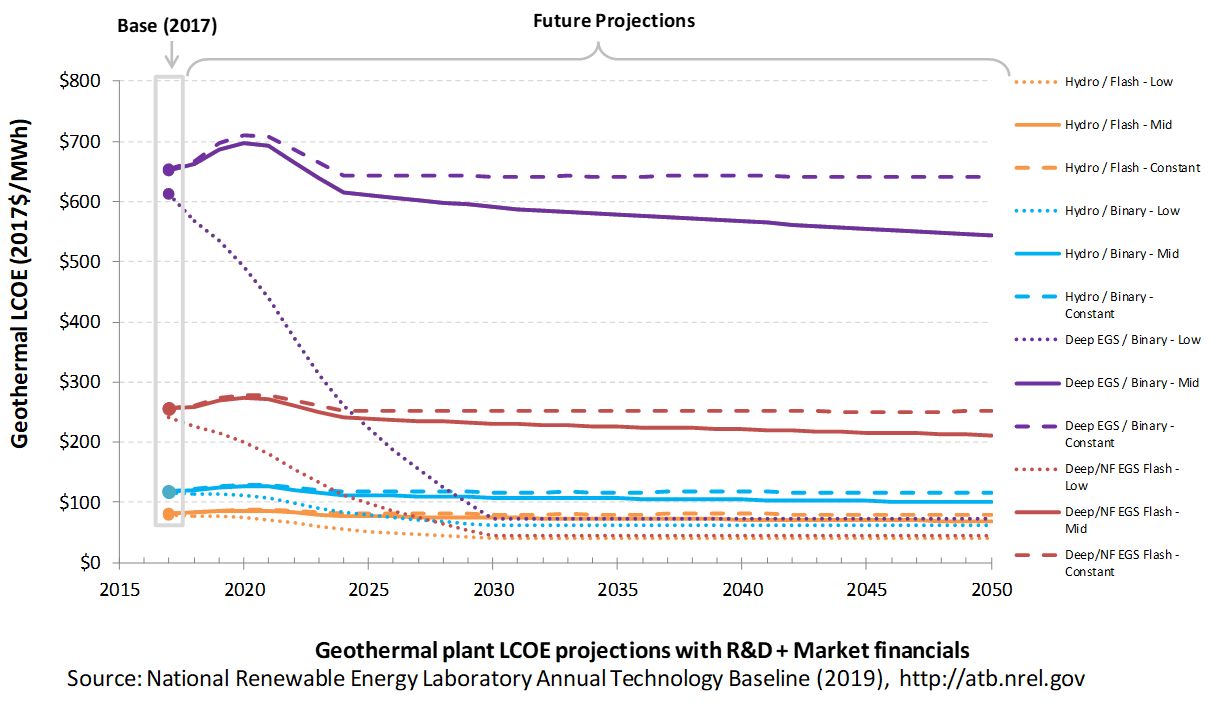

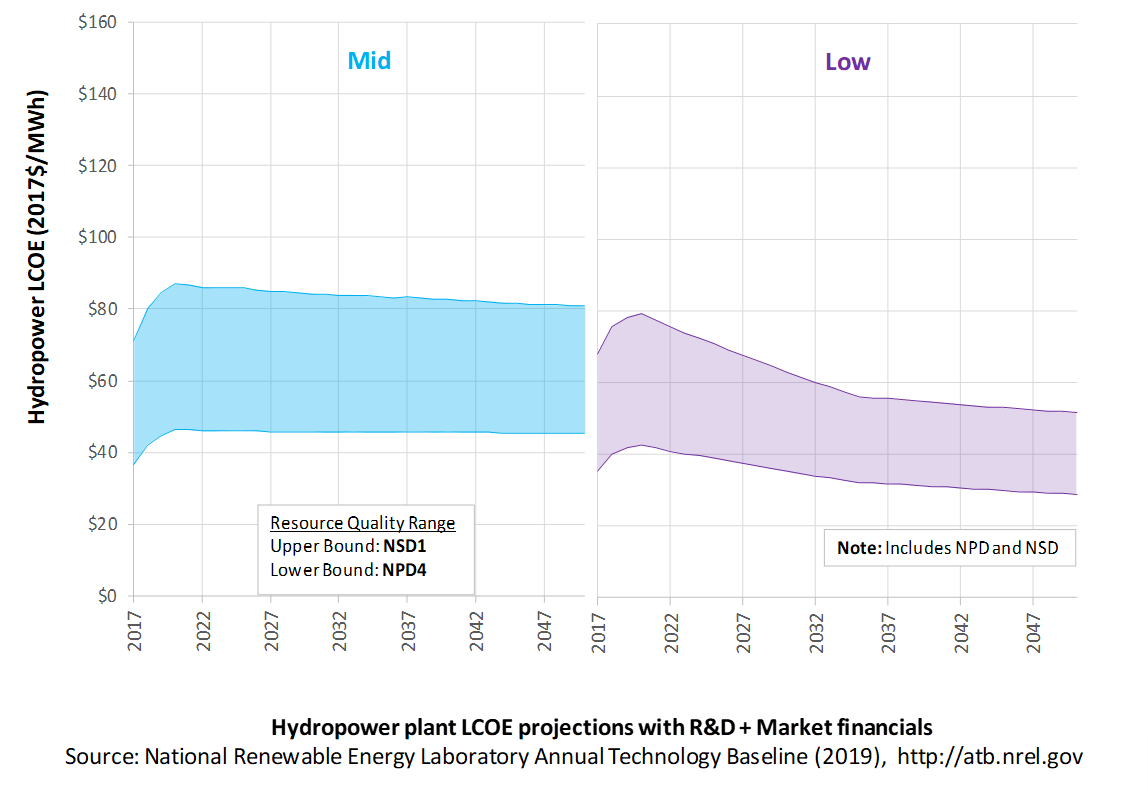

The following three figures illustrate LCOE, which includes the combined impact of CAPEX, O&M, and capacity factor projections for residential PV across the range of resources present in the contiguous United States. For the purposes of the ATB, the costs associated with technology and project risk in the U.S. market are represented in the financing costs but not in the upfront capital costs (e.g., developer fees and contingencies). An individual technology may receive more favorable financing terms outside of the United States, due to less technology and project risk, caused by more project development experience (e.g., offshore wind in Europe) or more government or market guarantees. The R&D Only LCOE sensitivity cases present the range of LCOE based on financial conditions that are held constant over time unless R&D affects them, and they reflect different levels of technology risk. This case excludes effects of tax reform, tax credits, and changing interest rates over time. The R&D + Market LCOE case adds to these financial assumptions: (1) the changes over time consistent with projections in the Annual Energy Outlook and (2) the effects of tax reform and tax credits. The ATB representative plant characteristics that best align with those of recently installed or anticipated near-term residential PV plants are associated with Res PV: Kansas City. Data for all the resource categories can be found in the ATB Data spreadsheet; for simplicity, not all resource categories are shown in the figures. In the R&D + Market LCOE case, there is an increase in LCOE from 2018-2020, caused by an increase WACC, and an increase from 2023-2024, caused by the reduction in tax credits.

R&D Only | R&D + Market

The methodology for representing the CAPEX, O&M, and capacity factor assumptions behind each pathway is discussed in Projections Methodology. In general, the degree of adoption of technology innovation distinguishes the Constant, Mid, and Low technology cost scenarios. These projections represent trends that reduce CAPEX and improve performance. Development of these scenarios involves technology-specific application of the following general definitions:

- Constant Technology Cost Scenario: Base Year (or near-term estimates of projects under construction) equivalent through 2050 maintains current relative technology cost differences

- Mid Technology Cost Scenario: Technology advances through continued industry growth, public and private R&D investments, and market conditions relative to current levels that may be characterized as "likely" or "not surprising"

- Low Technology Cost Scenario: technology advances that may occur with breakthroughs, increased public and private R&D investments, and/or other market conditions that lead to cost and performance levels that may be characterized as the "limit of surprise" but not necessarily the absolute low bound.

To estimate LCOE, assumptions about the cost of capital to finance electricity generation projects are required, and the LCOE calculations are sensitive to these financial assumptions. Two project finance structures are used within the ATB:

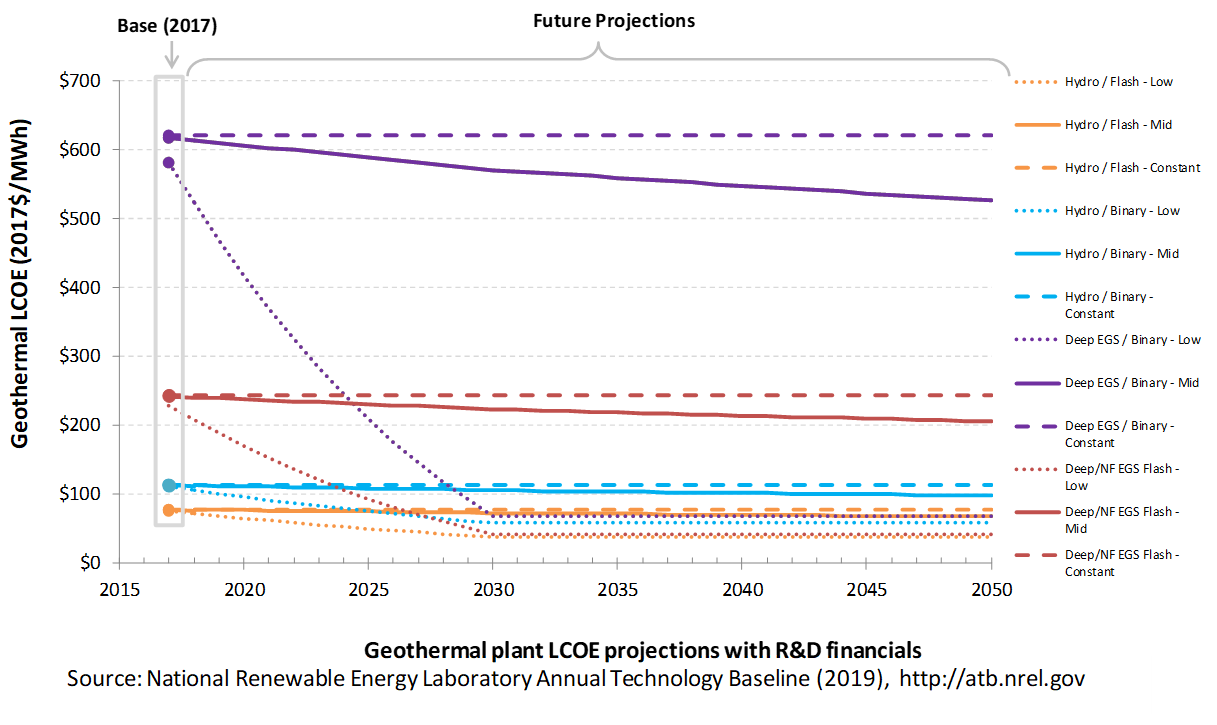

- R&D Only Financial Assumptions: This sensitivity case allows technology-specific changes to debt interest rates, return on equity rates, and debt fraction to reflect effects of R&D on technological risk perception, but it holds background rates constant at 2017 values from AEO 2019 (EIA 2019b) and excludes effects of tax reform and tax credits.

- R&D Only + Market Financial Assumptions: This sensitivity case retains the technology-specific changes to debt interest, return on equity rates, and debt fraction from the R&D Only case and adds in the variation over time consistent with AEO2019 as well as effects of tax reform and tax credits. For a detailed discussion of these assumptions, see Project Finance Impact on LCOE.

A constant cost recovery period – over which the initial capital investment is recovered – of 30 years is assumed for all technologies throughout this website, and can be varied in the ATB data spreadsheet.

The equations and variables used to estimate LCOE are defined on the Equations and Variables page. For illustration of the impact of changing financial structures such as WACC, see Project Finance Impact on LCOE. For LCOE estimates for the Constant, Mid, and Low technology cost scenarios for all technologies, see 2019 ATB Cost and Performance Summary.

In general, differences among the technology cost cases reflect different levels of adoption of innovations. Reductions in technology costs reflect the cost reduction opportunities that are listed below.

The LCOE for residential PV systems is calculated using the same financing parameters as the utility systems. Although we recognize that residential systems have a wide range of financing options available to them (e.g., cash payment, loan, and lease), we represent LCOEs using these utility-based financing calculations in order to allow better comparison against the utility system LCOEs.

- Modules

- Increased module efficiencies and increased production-line throughput to decrease CAPEX; overhead costs on a per-kilowatt basis will go down if efficiency and throughput improvement are realized

- Reduced wafer thickness or the thickness of thin-film semiconductor layers

- Development of new semiconductor materials

- Development of larger manufacturing facilities in low-cost regions

- Balance of system (BOS)

- Increased module efficiency, reducing the size of the installation

- Development of racking systems that enhance energy production or require less robust engineering

- Integration of racking or mounting components in modules

- Reduction of supply chain complexity and cost

- Creation of standard packaged system design

- Improvement of supply chains for BOS components in modules

- Improved power electronics

- Improvement of inverter prices and performance, possibly by integrating microinverters

- Decreased installation costs and margins

- Reduction of supply chain margins (e.g., profit and overhead charged by suppliers, manufacturer, distributors, and retailers); this will likely occur naturally as the U.S. PV industry grows and matures

- Streamlining of installation practices through improved workforce development and training and developing standardized PV hardware

- Expansion of access to a range of innovative financing approaches and business models

- Development of best practices for permitting interconnection and PV installation such as subdivision regulations, new construction guidelines, and design requirements.

FOM cost reduction represents optimized O&M strategies, reduced component replacement costs, and lower frequency of component replacement.

Geothermal

Geothermal technology cost and performance projections have been updated with analysis and results from the GeoVision: Harnessing the Heat Beneath our Feet report (DOE, 2019). The GeoVision report is a collaborative multiyear effort with contributors from industry, academia, national laboratories, and federal agencies. The analysis in the report updates resource potential estimates as well as current and projected capital and O&M costs based on rigorous, bottom-up modeling.

Representative Technology

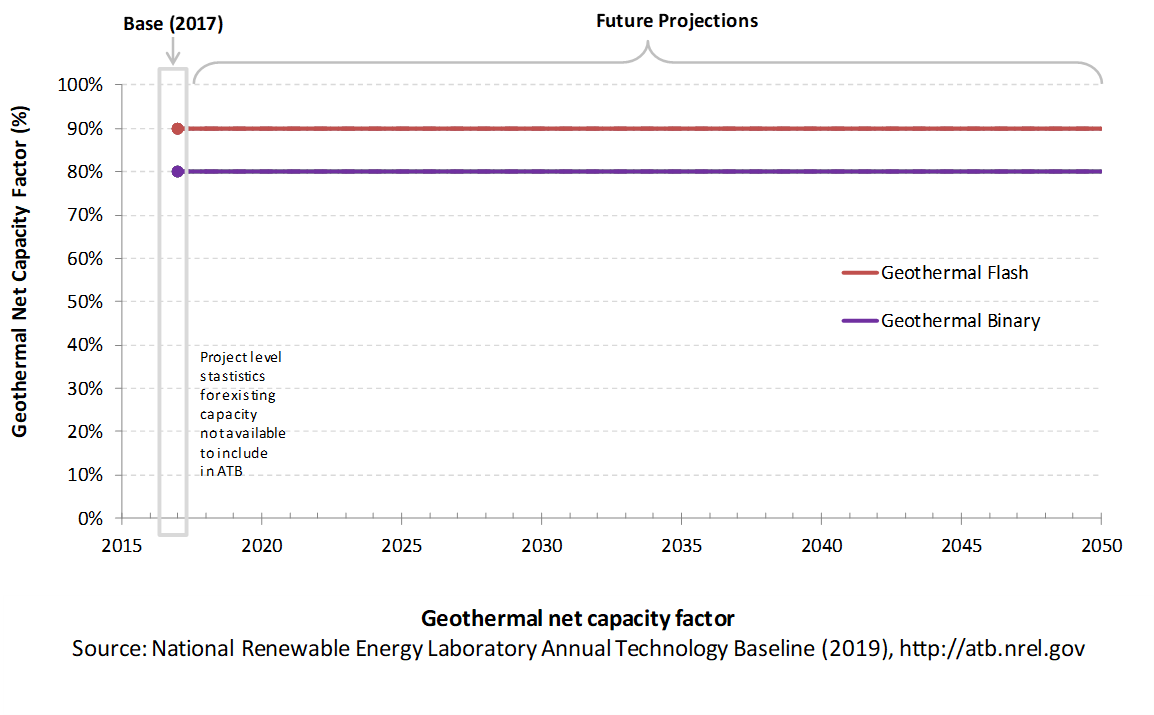

Hydrothermal geothermal technologies encompass technologies for exploring for the resource, drilling to access the resource, and building power plants to convert geothermal energy to electricity. Technology costs depend heavily on the hydrothermal resource temperature and well productivity and depth, so much so that project costs are site-specific and applying a "typical" cost to any given site would be inaccurate. The 2019 ATB uses scenarios developed by the DOE Geothermal Technology Office (Mines, 2013) for representative binary and flash hydrothermal power plant technologies. The first scenario assumes a 175°C resource at a depth of 1.5 km with wells producing an average of 110 kg/s of geothermal brine supplied to a 30-MWe binary (organic Rankine cycle) power plant. The second scenario assumes a 225°C resource at a depth of 2.5 km with wells producing 80 kg/s of geothermal brine supplied to a 40-MWe dual-flash plant. These are mid-grade or "typical" temperatures and depths for binary and flash hydrothermal projects. The ReEDS model uses the full hydrothermal supply curve. The 2019 ATB representative technologies fall in the middle or near the end of the hydrothermal resources typically deployed in ReEDS model runs.

Resource Potential

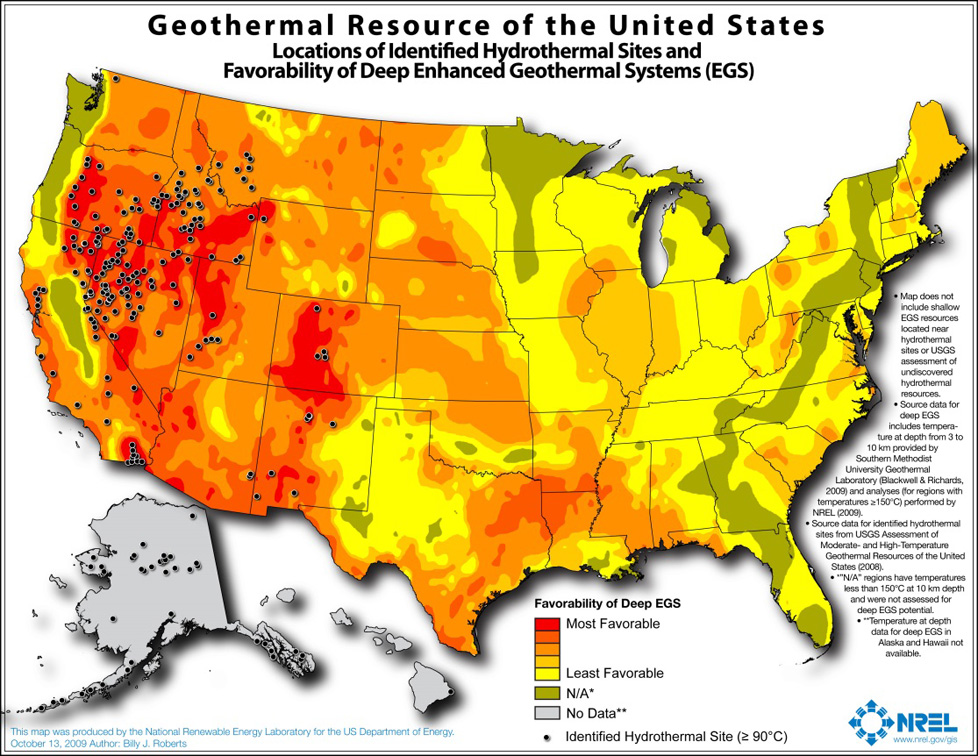

The hydrothermal geothermal resource is concentrated in the western United States. The total mean potential is 39,090 MW: 9,057 MW identified and 30,033 MW undiscovered (USGS, 2008). The resource potential identified by the U.S. Geological Survey (USGS, 2008) at each site is based on available reservoir thermal energy information from studies conducted at the site. The undiscovered hydrothermal technical potential estimate is based on a series of GIS statistical models for the spatial correlation of geological factors that facilitate the formation of geothermal systems.

The U.S. Geological Survey resource potential estimates for hydrothermal were used with the following modifications:

- Installed capacity of about 3 GW in 2016 is excluded from the resource potential.

- Resources on federally protected and U.S. Department of Defense (DOD) lands, where development is highly restricted are excluded from the resource potential, as are resources on lands where significant barriers that prevent or inhibit development of geothermal projects were identified by Augustine, Ho, and Blair (2019).

Renewable energy technical potential, as defined by Lopez et al. (2012), represents the achievable energy generation of a particular technology given system performance, topographic limitations, and environmental and land-use constraints. The primary benefit of assessing technical potential is that it establishes an upper-boundary estimate of development potential. It is important to understand that there are multiple types of potential-resource, technical, economic, and market (see NREL: "Renewable Energy Technical Potential").

Base Year and Future Year Projections Overview

The Base Year cost and performance estimates are calculated using Geothermal Electricity Technology Evaluation Model (GETEM), a bottom-up cost analysis tool that accounts for each phase of development of a geothermal plant (DOE "Geothermal Electricity Technology Evaluation Model").

- Cost and performance data for hydrothermal generation plants are estimated for each potential site using GETEM. Model results are based on resource attributes (e.g., estimated reservoir temperature, depth, and potential) of each site. GETEM inputs are derived from the Business-as-Usual (BAU) scenario from GeoVision ( (DOE, 2019), (Augustine, Ho, & Blair, 2019)).

- Site attribute values are from (USGS, 2008) for identified resource potential and from capacity-weighted averages of site attribute values of nearby identified resources for undiscovered resource potential.

- GETEM is used to estimate CAPEX, O&M, and parasitic plant losses that affect net energy production.

Capacity factor and O&M costs for plants installed in future years are unchanged from the Base Year. Projections for hydrothermal and EGS technologies are equivalent.

- Constant Technology Cost Scenario: no change in CAPEX, O&M, or capacity factor from 2015 to 2050; consistent across all renewable energy technologies in the ATB

- Mid Technology Cost Scenario: CAPEX cost reduction based on assumed minimum learning as implemented in AEO (EIA, 2015): 10% by 2035; this corresponds to a 0.5% annual improvement in CAPEX, which is assumed to continue on through 2050

- Low Technology Cost Scenario: CAPEX based on the Technology Improvement scenario from GeoVision Study ( (DOE, 2019); (Augustine, Ho, & Blair, 2019)); cost and technology improvements change linearly from present values and are fully achieved by 2030.

Representative Technology

As with cost for projects that use hydrothermal resources, EGS resource project costs depend so heavily on the hydrothermal resource temperature and well productivity and depth that project costs are site-specific. The 2019 ATB uses scenarios developed by the DOE Geothermal Technology Office (Mines, 2013) for representative binary and flash EGS power plants assuming current (immature) EGS technology performance metrics. The first scenario assumes a 175°C resource at a depth of 3 km with wells producing an average of 40 kg/s of geothermal brine supplied to a 25-MWe binary (organic Rankine cycle) power plant. The second scenario assumes a 250°C resource at a depth of 3.5 km with wells producing 40 kg/s of geothermal brine supplied to a 30-MWe dual-flash plant. These temperatures and depths are at the low-cost end of the EGS supply curve and would be some of the first developed. The ReEDS model uses the full EGS supply curve. Neither of these technologies is typically used.

Resource Potential

The enhanced geothermal system (EGS) resource is concentrated in the western United States. The total potential is greater than 100,000 MW: 1,493 MW of near-hydrothermal field EGS (NF-EGS) and the remaining potential comes from deep EGS.

Renewable energy technical potential as defined by Lopez et al. (2012) represents the achievable energy generation of a particular technology given system performance, topographic limitations, environmental, and land-use constraints. The primary benefit of assessing technical potential is that it establishes an upper-boundary estimate of development potential. It is important to understand there are multiple types of potential-resource, technical, economic, and market (see NREL: "Renewable Energy Technical Potential").

Base Year and Future Year Projections Overview

The Base Year cost and performance estimates are calculated using the Geothermal Electricity Technology Evaluation Model (GETEM), a bottom-up cost analysis tool that accounts for each phase of development of a geothermal plant (DOE "Geothermal Electricity Technology Evaluation Model").

- Cost and performance data for EGS generation plants are estimated for each potential site using GETEM. Model results based on resource attributes (e.g., estimated reservoir temperature, depth, and potential) of each site. GETEM inputs are derived from the GeoVision BAU scenario ( (DOE, 2019), (Augustine, Ho, & Blair, 2019)).

- Approaches to restrict resource potential to about 500 GW based on USGS analysis may be implemented in the future.

- GETEM is used to estimate CAPEX and O&M and parasitic plant losses that affect net energy production.

Capacity factor and O&M costs for plants installed in future years are unchanged from the Base Year. Projections for hydrothermal and enhanced geothermal system technologies are equivalent.

- Constant Technology Cost Scenario: no change in CAPEX, O&M, or capacity factor from 2015 to 2050, consistent across all renewable energy technologies in the ATB

- Mid Technology Cost Scenario: CAPEX cost reduction based on assumed minimum learning as implemented in AEO (EIA, 2015): 10% by 2035; this corresponds to a 0.5% annual improvement in CAPEX, which is assumed to continue on through 2050.

- Low Technology Cost Scenario: CAPEX based on the GeoVision Technology Improvement scenario ( (DOE, 2019), (Augustine, Ho, & Blair, 2019)). Cost and technology improvements decrease linearly from present values and are fully achieved by 2030.

Capital expenditures (CAPEX) are expenditures required to achieve commercial operation in a given year. These expenditures include the geothermal generation plant, the balance of system (e.g., site preparation, installation, and electrical infrastructure), and financial costs (e.g., development costs, onsite electrical equipment, and interest during construction) and are detailed in CAPEX Definition. In the ATB, CAPEX reflects typical plants and does not include differences in regional costs associated with labor, materials, taxes, or system requirements. The related Standard Scenarios product uses Regional CAPEX Adjustments. The range of CAPEX demonstrates variation with resource in the contiguous United States.

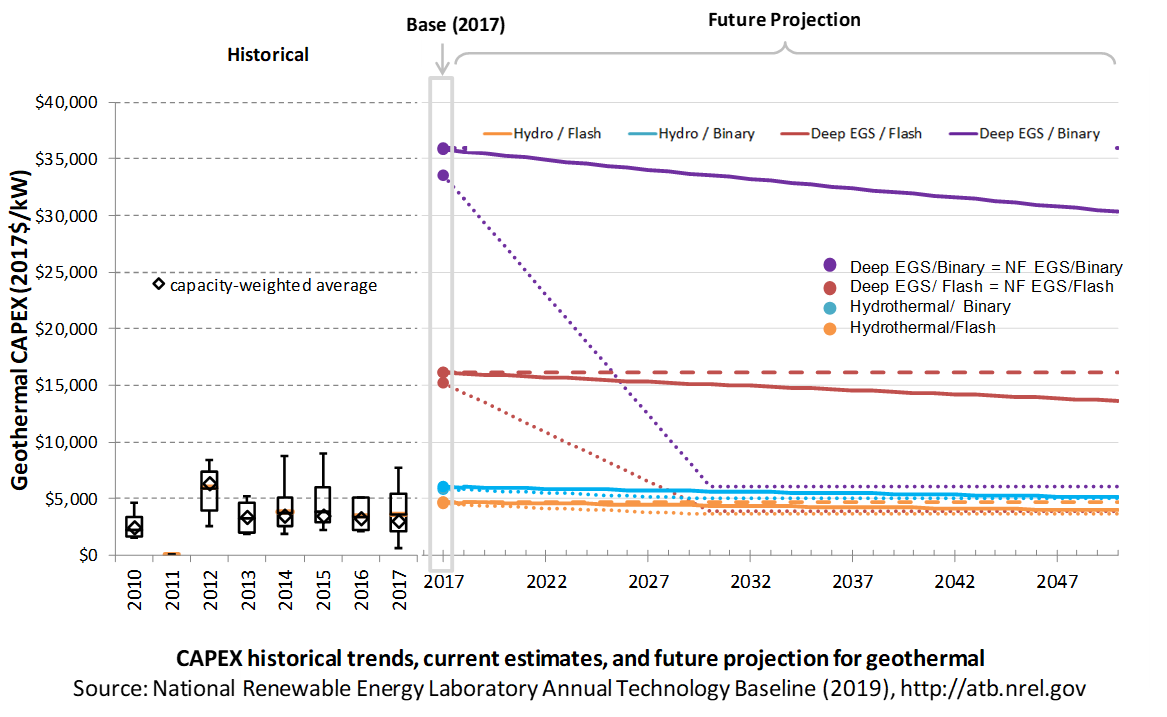

The following figure shows the Base Year estimate and future year projections for CAPEX costs. Three cost scenarios are represented: Constant, Mid, and Low technology cost. The estimate for a given year represents CAPEX of a new plant that reaches commercial operation in that year.

Base Year Estimates

For illustration in the ATB, six representative geothermal plants are shown. Two energy conversion processes are common: binary organic Rankine cycle and flash.

- Binary plants use a heat exchanger to transfer geothermal energy to an organic Rankine cycle. This technology generally applies to lower-temperature systems. These systems have higher CAPEX than flash systems because of the increased number of components, their lower-temperature operation, and a general requirement that a number of wells be drilled for a given power output.

- Flash plants create steam directly from the thermal fluid through a pressure change. This technology generally applies to higher-temperature systems. Due to the reduced number of components and higher-temperature operation, these systems generally produce more power per well, thus reducing drilling costs. These systems generally have lower CAPEX than binary systems.

Examples using each of these plant types in each of the three resource types (hydrothermal, NF-EGS, and deep EGS) are shown in the ATB.

Costs are for new or greenfield hydrothermal projects, not for re-drilling or additional development/capacity additions at an existing site.

Characteristics for the six examples of plants representing current technology were developed based on discussion with industry stakeholders. The CAPEX estimates were generated using GETEM. CAPEX for NF-EGS and EGS are equivalent.

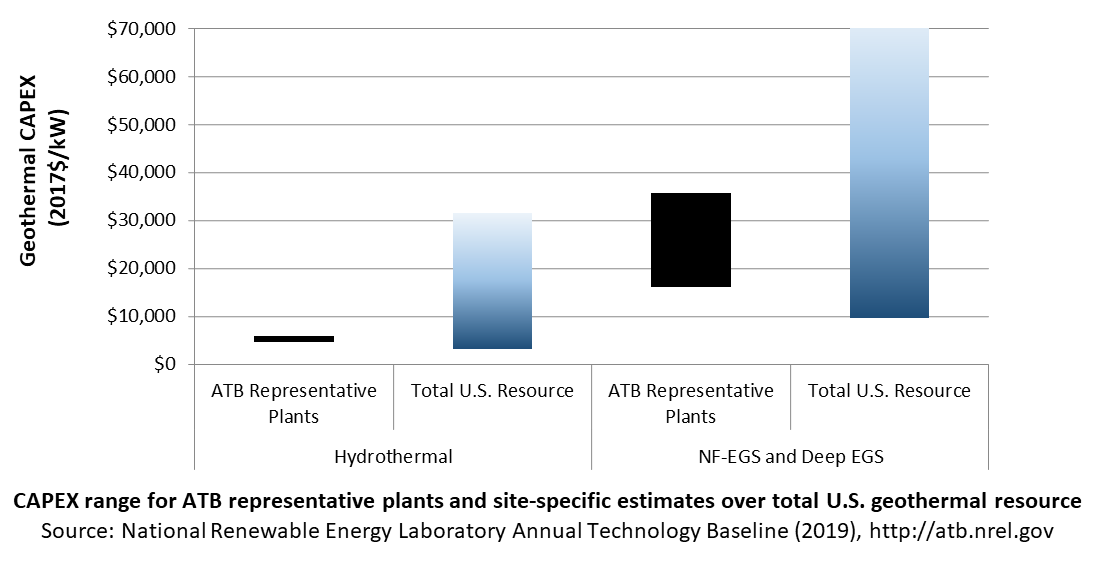

The following table shows the range of OCC associated with the resource characteristics for potential sites throughout the United States.

| Temp (°C) | >=200C | 150-200 | 135-150 | <135 | |

| Hydrothermal | Number of identified sites | 21 | 23 | 17 | 59 |

| Total capacity (MW) | 15,338 | 2,991 | 820 | 4,632 | |

| Average OCC ($/kW) | 3,906 | 7,720 | 8,794 | 16,248 | |

| Min OCC ($/kW) | 3,000 | 4,140 | 7,004 | 10,950 | |

| Max OCC ($/kW) | 5,491 | 29,135 | 11,027 | 21,349 | |

| Example of plant OCC ($/kW) | 4,229 | 5,455 | |||

| NF-EGS | Number of sites | 12 | 20 | ||

| Total capacity (MW) | 787 | 596 | |||

| Average OCC ($/kW) | 11,041 | 26,077 | |||

| Min OCC ($/kW) | 8,778 | 18,172 | |||

| Max OCC ($/kW) | 18,009 | 39,987 | |||

| Example of plant OCC ($/kW) | 14,512 | 32,268 | |||

| Deep EGS (3-6 km) | Number of sites | n/a | n/a | ||

| Total capacity (MW) | 100,000+ | ||||

| Average OCC ($/kW) | 28,418 | 60,170 | |||

| Min OCC ($/kW) | 18,320 | 39,329 | |||

| Max OCC ($/kW) | 54,047 | 77,983 | |||

| Example of plant OCC ($/kW) | 14,512 | 32,268 | |||

Future Year Projections

Projection of future geothermal plant CAPEX for the Low case is based on the GeoVision Technology Improvement scenario (DOE, 2019).

A detailed description of the methodology for developing future year projections is found in Projections Methodology.

Technology innovations that could impact future O&M costs are summarized in LCOE Projections.

CAPEX Definition

Capital expenditures (CAPEX) are expenditures required to achieve commercial operation in a given year.

For the ATB – and based on (EIA, 2016) and GETEM component cost calculations – the geothermal plant envelope is defined to include:

- Geothermal generation plant

- Exploration, confirmation drilling, well field development, reservoir stimulation (EGS), plant equipment, and plant construction

- Power plant equipment, well-field equipment, and components for wells (including dry/non-commercial wells)

- Balance of system (BOS)

- Installation and electrical infrastructure, such as transformers, switchgear, and electrical system connecting turbines to each other and to the control center

- Project indirect costs, including costs related to engineering, distributable labor and materials, construction management start up and commissioning, and contractor overhead costs, fees, and profit

- Financial costs

- Owners' costs, such as development costs, preliminary feasibility and engineering studies, environmental studies and permitting, legal fees, insurance costs, and property taxes during construction

- Electrical interconnection and onsite electrical equipment (e.g., switchyard), a nominal-distance spur line (<1 mile), and necessary upgrades at a transmission substation; distance-based spur line cost (GCC) not included in the ATB

- Interest during construction estimated based on four-year and five-year duration for hydrothermal and EGS respectively (for the low scenario) and an eight-year duration and ten-year duration for hydrothermal and EGS respectively (for the mid- and constant-scenario) accumulated at different intervals for hydro and EGS based on scheduled at outlined by the GeoVision Study (ConFinFactor).

CAPEX can be determined for a plant in a specific geographic location as follows:

Regional cost variations and geographically specific grid connection costs are not included in the ATB (CapRegMult = 1; GCC = 0). In the ATB, the input value is overnight capital cost (OCC) and details to calculate interest during construction (ConFinFactor).

In the ATB, CAPEX is shown for six representative plants. Examples of CAPEX for binary organic Rankine cycle and flash energy conversion processes in each of three geothermal resource types are presented. CAPEX estimates for all hydrothermal NF-EGS potential results in a CAPEX range that is much broader than that shown in the ATB. It is unlikely that all the resource potential will be developed due to the high costs for some sites. Regional cost effects and distance-based spur line costs are not estimated.

Standard Scenarios Model Results

ATB CAPEX, O&M, and capacity factor assumptions for the Base Year and future projections through 2050 for Constant, Mid, and Low technology cost scenarios are used to develop the NREL Standard Scenarios using the ReEDS model. See ATB and Standard Scenarios.

The ReEDS model represents cost and performance for hydrothermal, NF-EGS, and EGS potential in 5 bins for each of 134 geographic regions, resulting in a greater CAPEX range in the reference supply curve than what is shown in examples in the ATB.

CAPEX in the ATB does not represent regional variants (CapRegMult) associated with labor rates, material costs, etc., and neither does the ReEDS model.

CAPEX in the ATB does not include geographically determined spur line (GCC) from plant to transmission grid, and neither does the ReEDS model.

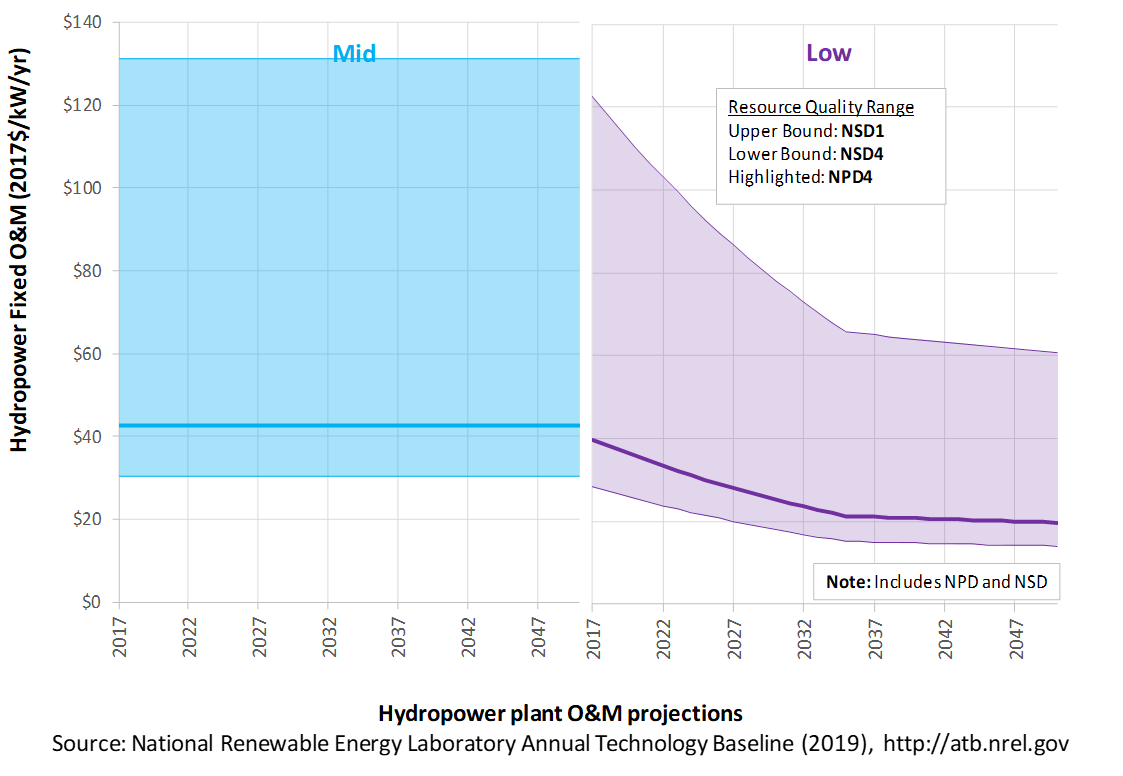

Operations and maintenance (O&M) costs represent average annual fixed expenditures (and depend on rated capacity) required to operate and maintain a hydrothermal plant over its lifetime of 30 years (plant and reservoir), including:

- Insurance, taxes, land lease payments, and other fixed costs

- Present value and annualized large component overhaul or replacement costs over technical life (e.g., downhole pumps)

- Scheduled and unscheduled maintenance of geothermal plant components and well field components over the technical lifetime of the plant and reservoir.

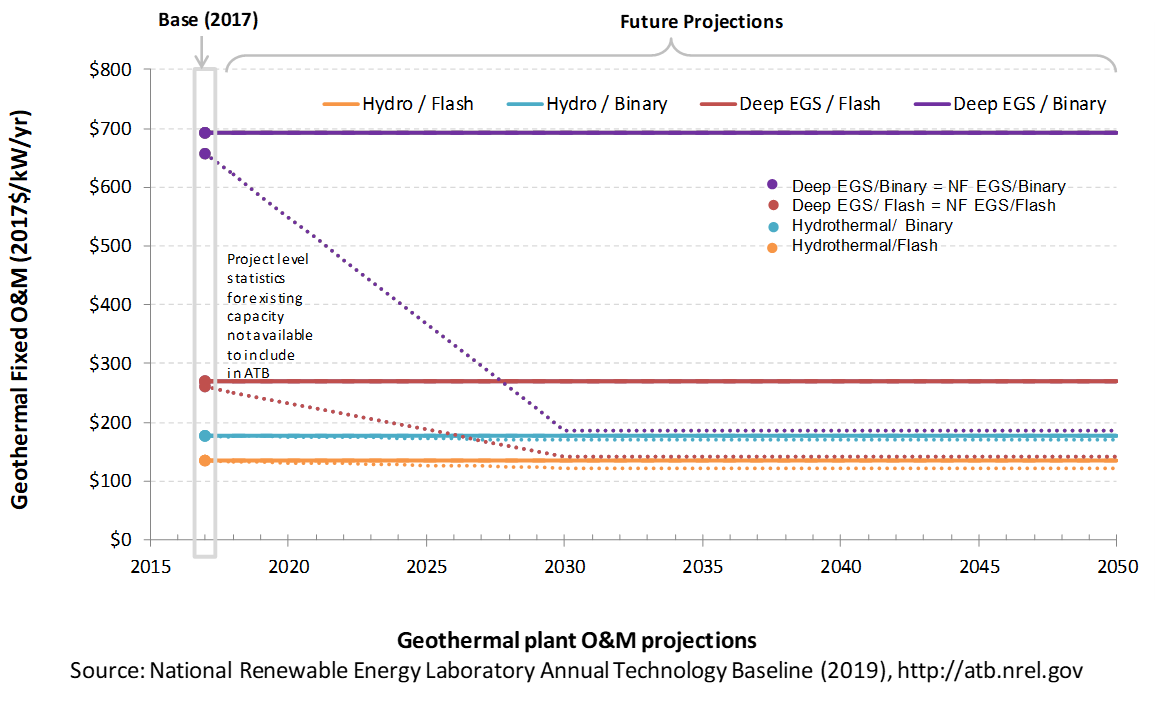

The following figure shows the Base Year estimate and future year projections for fixed O&M (FOM) costs. Three cost scenarios are represented. The estimate for a given year represents annual average FOM costs expected over the technical lifetime of a new plant that reaches commercial operation in that year.

Base Year Estimates

FOM is estimated for each example of a plant based on technical characteristics.

GETEM is used to estimate FOM for each of the six representative plants. FOM for NF-EGS and EGS are equivalent.

Future Year Projections

Future FOM cost reductions are based on results from the GeoVision scenario (DOE, 2019) and are described in detail in Augustine, Ho, and Blair (2019).

Capacity Factor: Expected Annual Average Energy Production Over Lifetime

The capacity factor represents the expected annual average energy production divided by the annual energy production, assuming the plant operates at rated capacity for every hour of the year. It is intended to represent a long-term average over the technical lifetime of the plant. It does not represent interannual variation in energy production. Future year estimates represent the estimated annual average capacity factor over the technical lifetime of a new plant installed in a given year.

Geothermal plant capacity factor is influenced by diurnal and seasonal air temperature variation (for air-cooled plants), technology (e.g., binary or flash), downtime, and internal plant energy losses.

The following figure shows a range of capacity factors based on variation in the resource for plants in the contiguous United States. The range of the Base Year estimates illustrates Binary or Flash geothermal plants. Future year projections for the Constant, Mid, and Low technology cost scenarios are unchanged from the Base Year. Technology improvements are focused on CAPEX cost elements.

Base Year Estimate

The capacity factor estimates are developed using GETEM at typical design air temperature and based on design plant capacity net losses. An additional reduction is applied to approximate potential variability due to seasonal temperature effects.

Some geothermal plants have experienced year-on-year reductions in energy production, but this is not consistent across all plants. No approximation of long-term degradation of energy output is assumed.

Ongoing work at NREL and the Idaho National Laboratory is helping improve capacity factor estimates for geothermal plants. As this work progresses, it will be incorporated into future versions of the ATB.

Future Year Projections

Capacity factors remain unchanged from the Base Year through 2050. Technology improvements are focused on CAPEX costs. Estimates of capacity factor for geothermal plants in the ATB represent typical operation. The dispatch characteristics of these systems are valuable to the electric system to manage changes in net electricity demand. Actual capacity factors will be influenced by the degree to which system operators call on geothermal plants to manage grid services.

Plant Cost and Performance Projections Methodology

The site-specific nature of geothermal plant cost, the relative maturity of hydrothermal plant technology, and the very early stage development of EGS technologies make cost projections difficult. No thorough literature reviews have been conducted for cost reduction of hydrothermal geothermal technologies or EGS technologies. However, the GeoVision BAU scenario is based on a bottom-up analysis of costs and performance improvements. The inputs for the BAU scenario were developed by the national laboratories as part of the GeoVision effort, and it was reviewed by industry experts.

Projection of future geothermal plant CAPEX for the Low cost case is based on the GeoVision Technology Improvement scenario. It assumes that cost and technology improvements are achieved by 2030 and that costs decrease linearly from present values to the 2030 projected values. The Mid cost case is based on minimum learning rates as implemented in AEO (EIA, 2015): 10% by 2035. This corresponds to a 0.5% annual improvement in CAPEX, which is assumed to continue on through 2050. The Constant technology cost scenario retains all cost and performance assumptions equivalent to the Base Year through 2050.

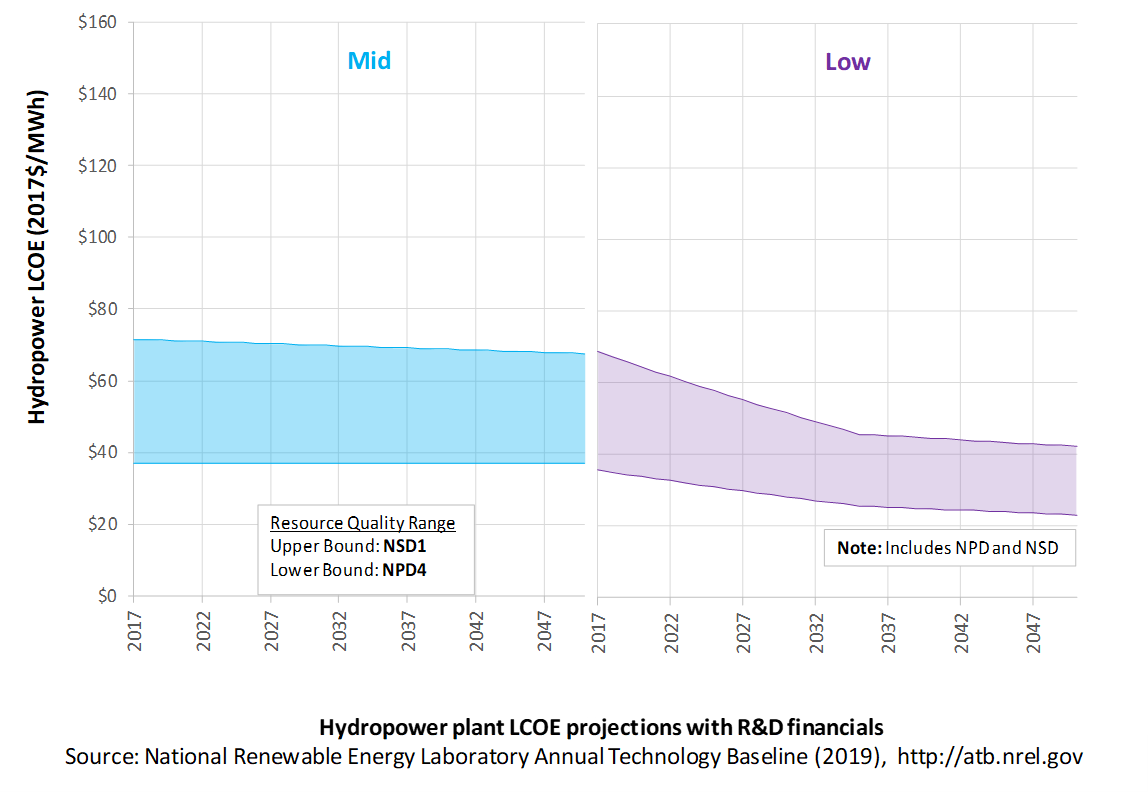

Levelized Cost of Energy (LCOE) Projections

Levelized cost of energy (LCOE) is a simple metric that combines the primary technology cost and performance parameters: CAPEX, O&M, and capacity factor. It is included in the ATB for illustrative purposes. The ATB focuses on defining the primary cost and performance parameters for use in electric sector modeling or other analysis where more sophisticated comparisons among technologies are made. The LCOE accounts for the energy component of electric system planning and operation. The LCOE uses an annual average capacity factor when spreading costs over the anticipated energy generation. This annual capacity factor ignores specific operating behavior such as ramping, start-up, and shutdown that could be relevant for more detailed evaluations of generator cost and value. Electricity generation technologies have different capabilities to provide such services. For example, wind and PV are primarily energy service providers, while the other electricity generation technologies such as geothermal, can provide capacity and flexibility services in addition to energy. These capacity and flexibility services are difficult to value and depend strongly on the system in which a new generation plant is introduced. These services are represented in electric sector models such as the ReEDS model and corresponding analysis results such as the Standard Scenarios.

The following three figures illustrate LCOE, which includes the combined impact of CAPEX, O&M, and capacity factor projections for geothermal across the range of resources present in the contiguous United States. For the purposes of the ATB, the costs associated with technology and project risk in the U.S. market are represented in the financing costs but not in the upfront capital costs (e.g., developer fees and contingencies). An individual technology may receive more favorable financing terms outside the United States, due to less technology and project risk, caused by more project development experience (e.g., offshore wind in Europe) or more government or market guarantees. The R&D Only LCOE sensitivity cases present the range of LCOE based on financial conditions that are held constant over time unless R&D affects them, and they reflect different levels of technology risk. This case excludes effects of tax reform, tax credits, technology-specific tariffs, and changing interest rates over time. The R&D + Market LCOE case adds to these financial assumptions: (1) the changes over time consistent with projections in the Annual Energy Outlook and (2) the effects of tax reform, tax credits, and tariffs. The ATB representative plant characteristics that best align with those of recently installed or anticipated near-term geothermal plants are associated with Hydrothermal/Flash. Data for all the resource categories can be found in the ATB Data spreadsheet; for simplicity, not all resource categories are shown in the figures.

R&D Only | R&D + Market

The methodology for representing the CAPEX, O&M, and capacity factor assumptions behind each pathway is discussed in Projections Methodology. In general, the degree of adoption of technology innovation distinguishes the Constant, Mid, and Low technology cost scenarios. These projections represent trends that reduce CAPEX and improve performance. Development of these scenarios involves technology-specific application of the following general definitions:

- Constant Technology: Base Year (or near-term estimates of projects under construction) equivalent through 2050 maintains current relative technology cost differences

- Mid Technology Cost Scenario: Technology advances through continued industry growth, public and private R&D investments, and market conditions relative to current levels that may be characterized as "likely" or "not surprising"

- Low Technology Cost Scenario: Technology advances that may occur with breakthroughs, increased public and private R&D investments, and/or other market conditions that lead to cost and performance levels that may be characterized as the " limit of surprise" but not necessarily the absolute low bound.

To estimate LCOE, assumptions about the cost of capital to finance electricity generation projects are required, and the LCOE calculations are sensitive to these financial assumptions. Two project finance structures are used within the ATB:

- R&D Only Financial Assumptions: This sensitivity case allows technology-specific changes to debt interest rates, return on equity rates, and debt fraction to reflect effects of R&D on technological risk perception, but it holds background rates constant at 2017 values from AEO2019 (EIA, 2019) and excludes effects of tax reform, tax credits, and tariffs.

- R&D Only + Market Financial Assumptions: This sensitivity case retains the technology-specific changes to debt interest, return on equity rates, and debt fraction from the R&D Only case and adds in the variation over time consistent with AEO2018, as well as effects of tax reform, tax credits, and technology-specific tariffs. For a detailed discussion of these assumptions, see Changes from 2018 ATB to 2019 ATB.

A constant cost recovery period – over which the initial capital investment is recovered – of 30 years is assumed for all technologies throughout this website, and can be varied in the ATB data spreadsheet.

The equations and variables used to estimate LCOE are defined on the Equations and Variables page. For illustration of the impact of changing financial structures such as WACC, see Project Finance Impact on LCOE. For LCOE estimates for the Constant, Mid, and Low technology cost scenarios for all technologies, see 2019 ATB Cost and Performance Summary.

In general, differences among the technology cost cases reflect different levels of adoption of innovations. Reductions in technology costs reflect the cost reduction opportunities that are listed below.

- Development of exploration and reservoir characterization tools that reduce well-field costs through risk reduction by locating and characterizing low- and moderate-temperature hydrothermal systems prior to drilling

- High-temperature tools and electronics for geothermal subsurface operations

- Development of reservoir engineering techniques and technologies that enable EGS

- More efficient drilling practices and advanced drilling systems such as using flames or lasers to drill through rock; drilling steering technology; and other technologies to reduce drilling costs.

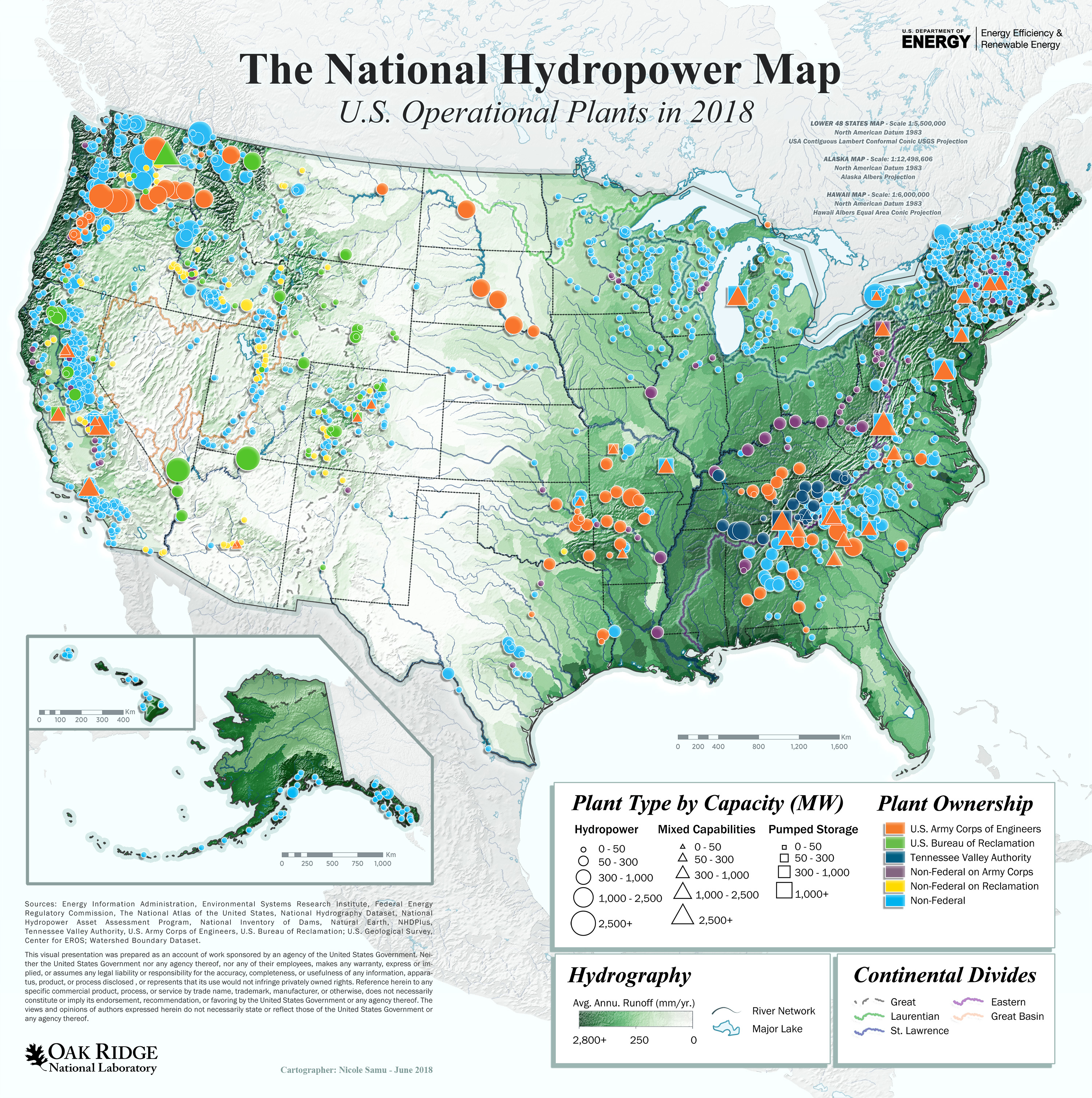

Hydropower

Renewable energy technical potential, as defined by Lopez et al. (2012) , represents the achievable energy generation of a particular technology given system performance, topographic limitations, and environmental and land-use constraints. The primary benefit of assessing technical potential is that it establishes an upper-boundary estimate of development potential. It is important to understand that there are multiple types of potential-resource, technical, economic, and market (see NREL: "Renewable Energy Technical Potential").

Note: Pumped-storage hydropower is considered a storage technology in the ATB and will be addressed in future years. It and other storage technologies are represented in Standard Scenarios Model Results from the ReEDS model, and battery storage technologies are shown in the associated portion of the ATB.

Representative Technology

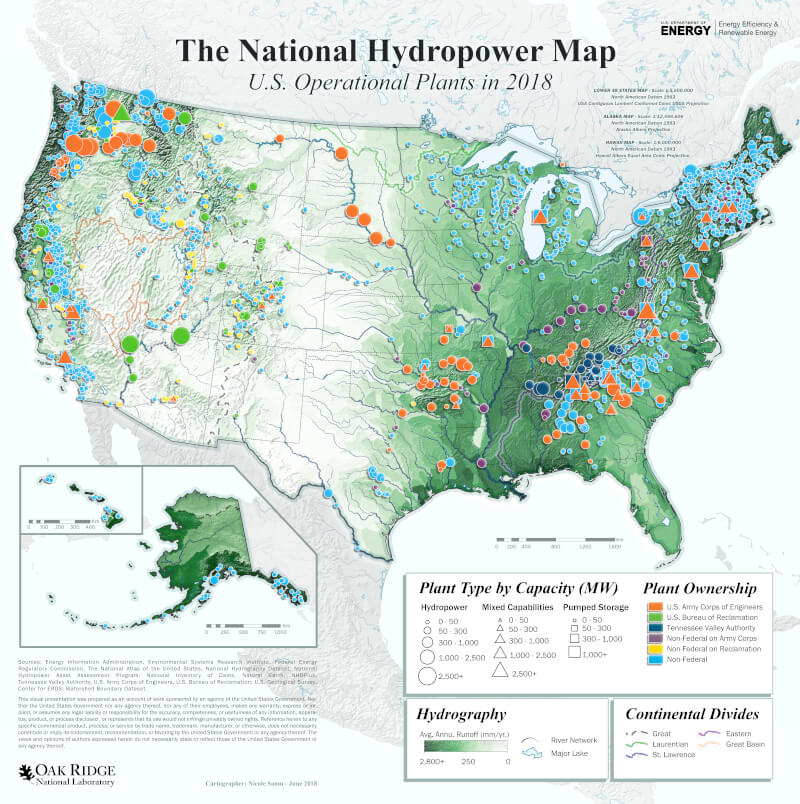

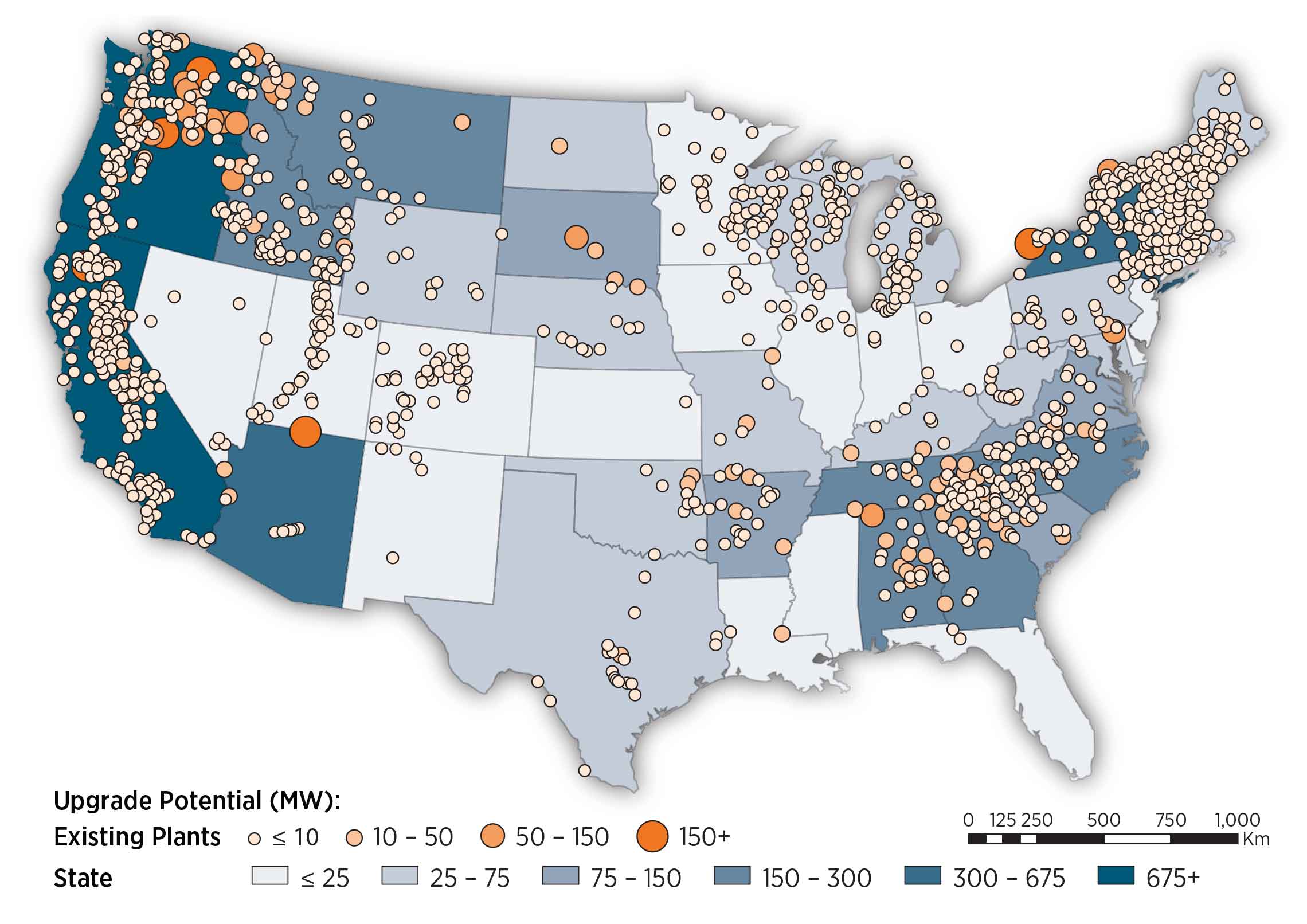

Hydropower technologies have produced electricity in the United States for over a century. Many of these infrastructure investments have potential to continue providing electricity in the future through upgrades of existing facilities (DOE, 2016) . At individual facilities, investments can be made to improve the efficiency of existing generating units through overhauls, generator rewinds, or turbine replacements. Such investments are known collectively as "upgrades," and they are reflected as increases to plant capacity. As plants reach a license renewal period, upgrades to existing facilities to increase capacity or energy output are typically considered. While the smallest projects in the United States can be as small as 10-100 kW, the bulk of upgrade potential is from large, multi-megawatt facilities.

Resource Potential

The estimated total upgrade potential of 6.9 GW/24 terawattt-hours (TWh) (at about 1,800 facilities) is based on generalizable information drawn from a series of case studies or owner-specific assessments (DOE, 2016) . Information available to inform the representation of improvements to the existing fleet includes:

- A systematic, full-fleet assessment of expansion potential at Reclamation projects performed under the Reclamation Hydropower Modernization Initiative (see U.S. Bureau of Reclamation, "Hydropower Resource Assessment at Existing Reclamation Facilities")

- Case study reports from the U.S. Army Corps of Engineers (Corps) performed under its Hydropower Modernization Initiative (MWH, Watson, & Harza, 2009)

- Case study reports combining assessments of upgrade and unit and plant optimization potential from the U.S. Department of Energy/Oak Ridge National Laboratory Hydropower Advancement Project.

{kind=link}

Base Year and Future Year Projections Overview

Upgrades are often among the lowest-cost new capacity resource, with the modeled costs for individual projects ranging from $800/kW to nearly $20,000/kW. This differential results from significant economies of scale from project size, wherein larger capacity plants are less expensive to upgrade on a dollar-per-kilowatt basis than smaller projects are. The average cost of the upgrade resource is approximately $1,500/kW.

CAPEX for each existing facility is based on direct estimates

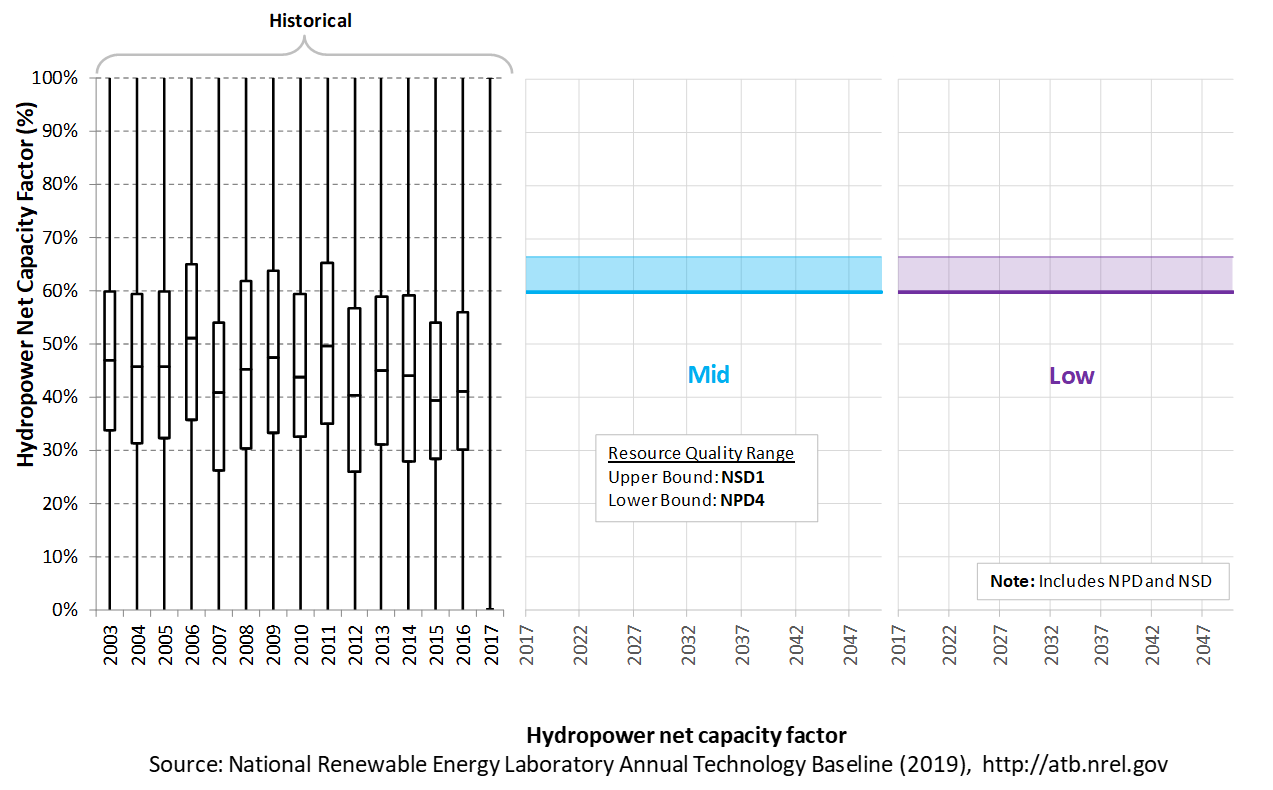

The capacity factor is based on actual 10-year average energy production reported in EIA 923 forms. Some hydropower facilities lack flexibility and only produce electricity when river flows are adequate. Others with storage capabilities are operated to meet a balance between electric system, reservoir management, and environmental needs using their dispatch capability.

No future cost and performance projections for hydropower upgrades are assumed.

Upgrade cost and performance are not illustrated in this documentation of the ATB for the sake of simplicity.

Standard Scenarios Model Results

ATB CAPEX, O&M, and capacity factor assumptions for the Base Year and future projections through 2050 for Constant, Mid, and Low technology cost scenarios are used to develop the NREL Standard Scenarios using the ReEDS model. See ATB and Standard Scenarios.

Upgrade potential becomes available in the ReEDS model at the relicensing date, end of plant life (50 years), or both.

Representative Technology

Non-powered dams (NPD) are classified by energy potential in terms of head. Low head facilities have design heads below 20 m and typically exhibit the following characteristics (DOE, 2016) :

- 1 MW to 10 MW

- New/rehabilitated intake structure

- Little, if any, new penstock

- Axial-flow or Kaplan turbines (2-4 units)

- New powerhouse (indoor)

- New/rehabilitated tailrace

- Minimal new transmission (< 5 miles, if required)

- Capacity factor of 35% to 60%.

High head facilities have design heads above 20 m and typically exhibit the following characteristics (DOE, 2016) :

- 5 MW to 30 MW

- New/rehabilitated intake structure

- New penstock (typically < 500 feet of steel penstock, if required)

- Francis turbines (1-3 units)

- New powerhouse (indoor)

- New/rehabilitated tailrace

- Minimal new transmission line (up to 15 MW, if required)

- Capacity factor of 35% to 60%.

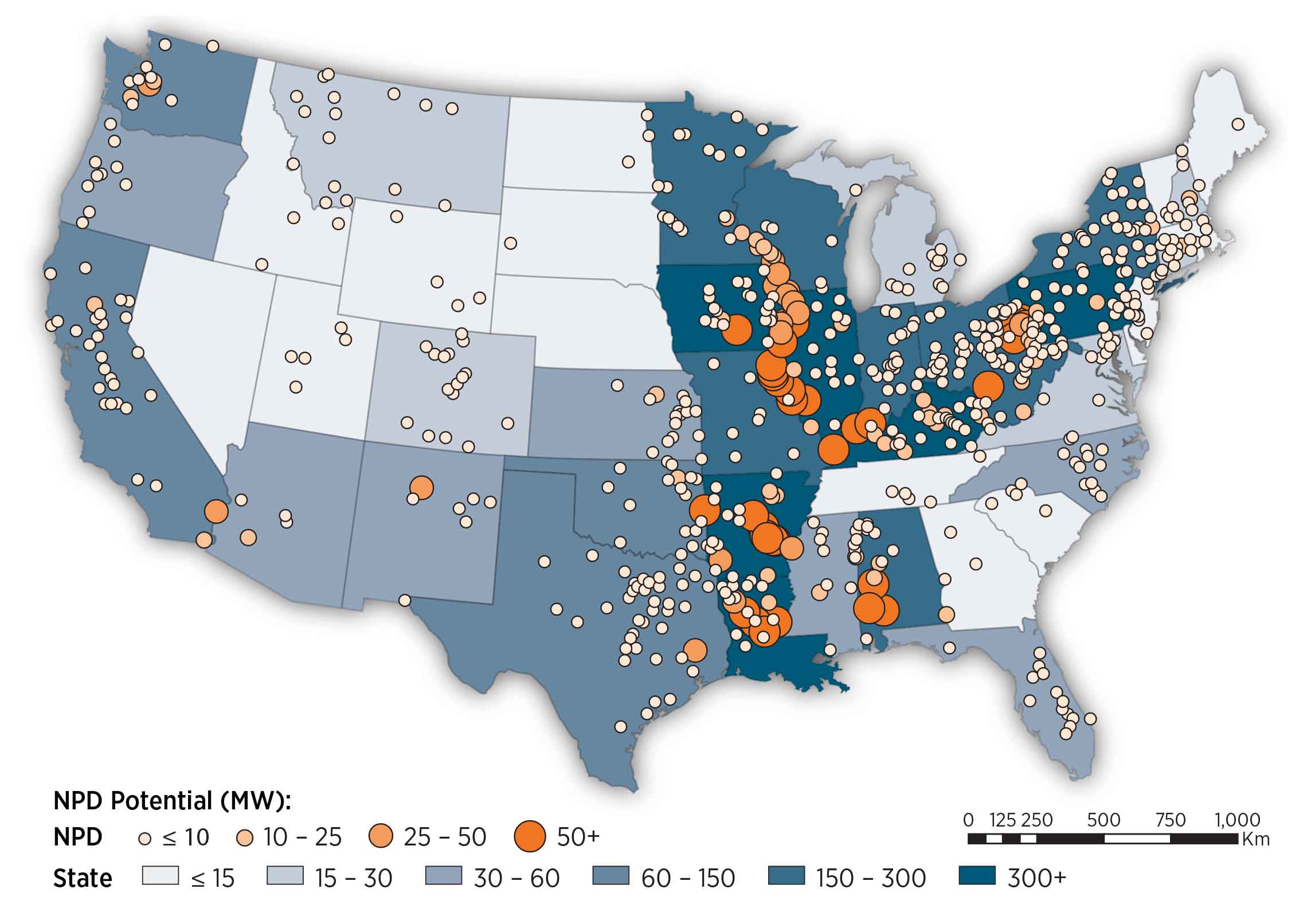

Resource Potential

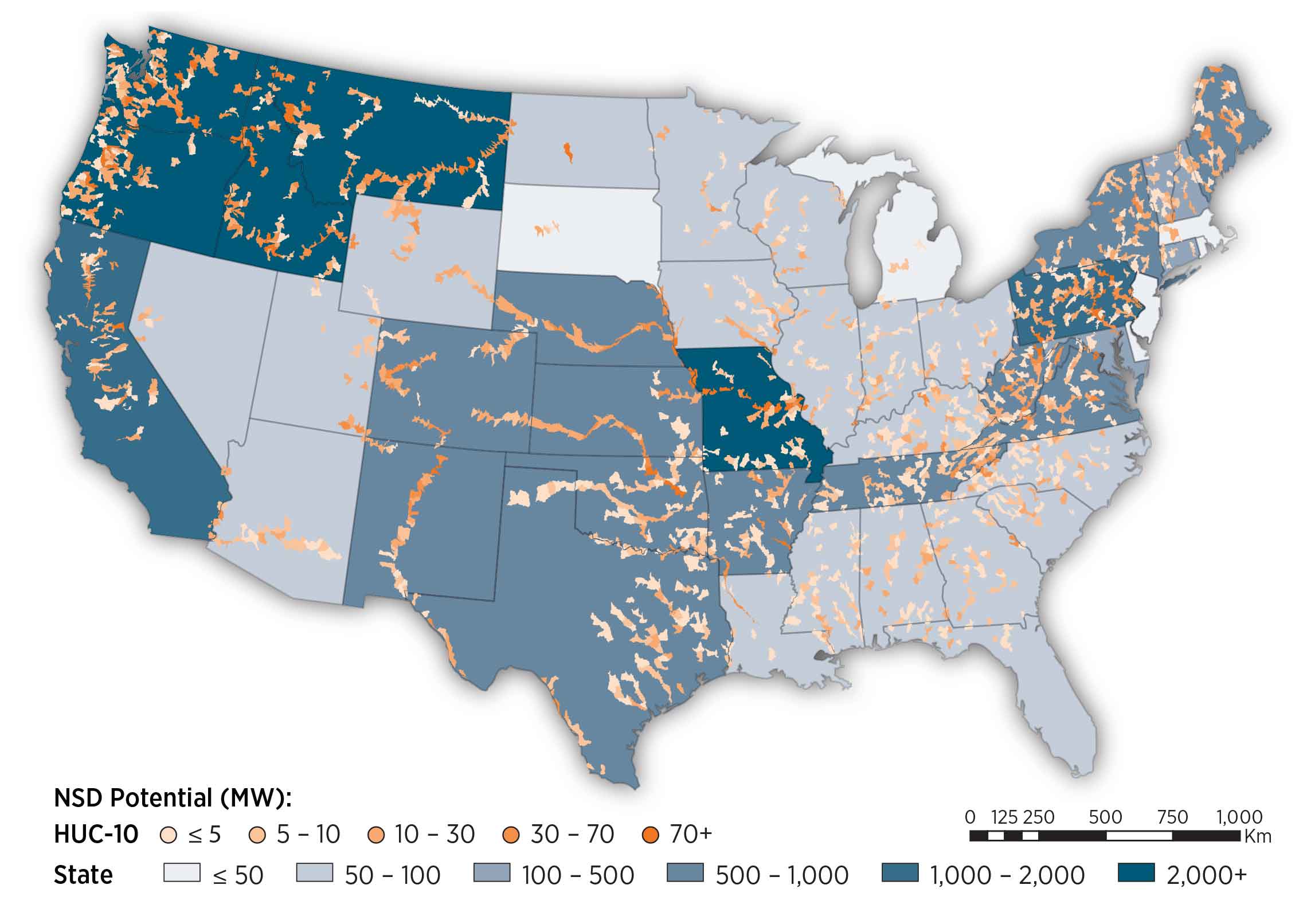

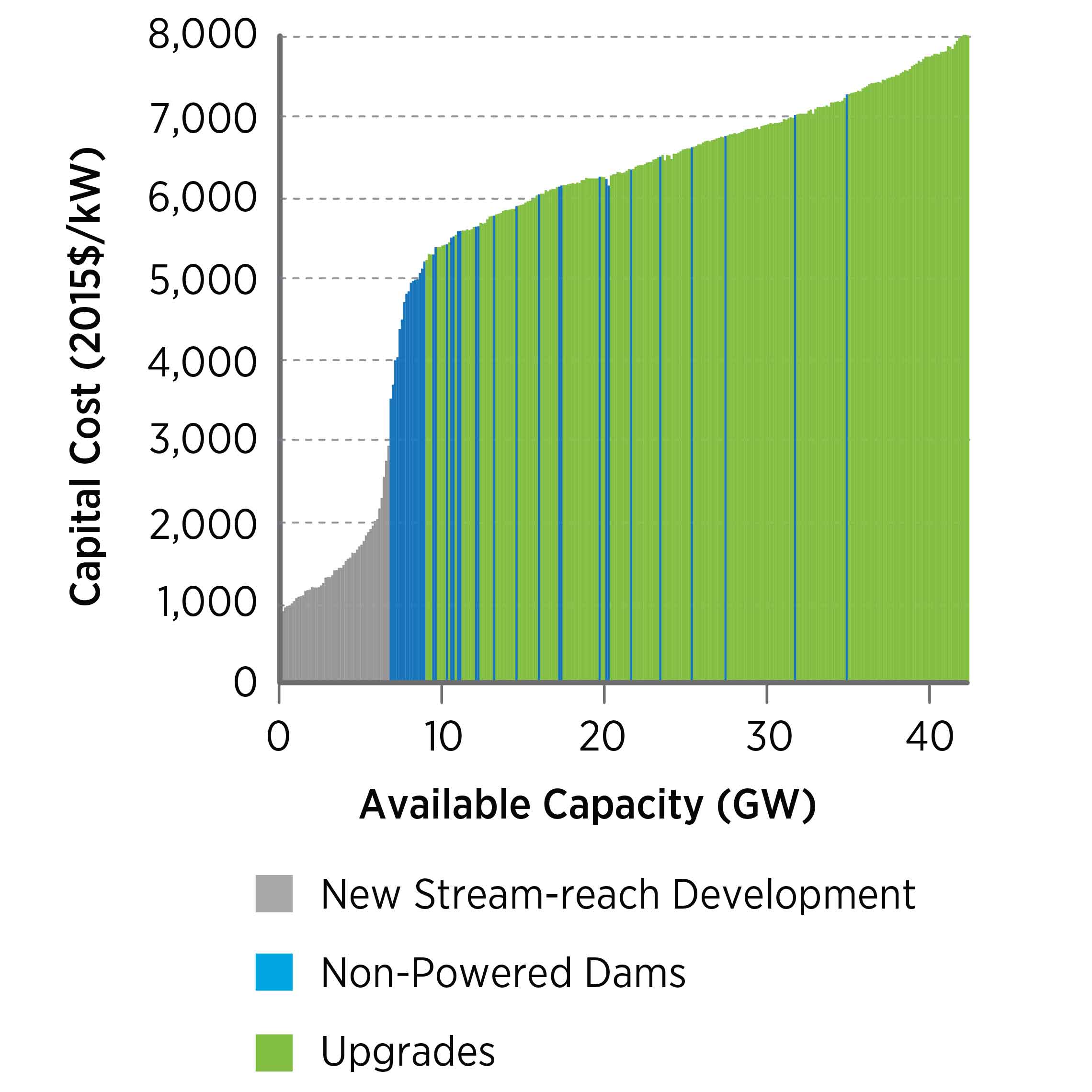

Up to 12 GW of technical potential exists to add power to U.S. NPD. However, based on financial decisions in recent development activity, the economic potential of NPD may be approximately 5.6 GW at more than 54,000 dams in the contiguous United States. Most of this potential (5 GW or 90% of resource capacity) is associated with less than 700 dams. These resource considerations are discussed below:

According to the National

Inventory of Dams, more than 80,000 dams exist that do not produce

power. This data set was filtered to remove dams with erroneous flow

and geographic data and dams whose data could not be resolved to a

satisfactory level of detail

A new methodology for sizing potential hydropower facilities that was developed for the new-stream reach development resource (Kao et al., 2014) was applied to non-powered dams. This resource potential was estimated to be 5.6 GW at more than 54,000 dams. In the development of the Hydropower Vision, the NPD resource available to the ReEDS model was adjusted based on recent development activity and limited to only those projects with power potential of 500 kW or more. As the ATB uses the Hydropower Vision supply curves, this results in a final resource potential of 5 GW/29 TWh from 671 dams.

For each facility, a design capacity, average monthly flow rate over a 30-year period, and a design flow rate exceedance level of 30% are assumed. The exceedance level represents the fraction of time that the design flow is exceeded. This parameter can be varied and results in different capacity and energy generation for a given site. The value of 30% was chosen based on industry rules of thumb. The capacity factor for a given facility is determined by these design criteria.

Design capacity and flow rate dictate capacity and energy generation potential. All facilities are assumed sized for 30% exceedance of flow rate based on long-term, average monthly flow rates.

Base Year and Future Year Projections Overview

Site-specific CAPEX, O&M, and capacity factor estimates are made

for each site in the available resource potential. CAPEX and O&M

estimates are made based on statistical analysis of historical plant

data from 1980 to 2015

Projections developed for the Hydropower Vision study (DOE, 2016) using technological learning assumptions and bottom-up analysis of process and/or technology improvements provide a range of future cost outcomes. Three different projections were developed for scenario modeling as bounding levels:

- Constant Technology Cost Scenario: no change in CAPEX, O&M, or capacity factor from 2017 to 2050; consistent across all renewable energy technologies in the ATB

- Mid Technology Cost Scenario: incremental technology learning, consistent with Reference in Hydropower Vision (DOE, 2016); CAPEX reductions for new stream-reach development (NSD) only

- Low cost: gains that are achievable when pushing to the limits of potential new technologies, such as modularity (in both civil structures and power train design), advanced manufacturing techniques, and materials, consistent with Advanced Technology in Hydropower Vision (DOE, 2016); both CAPEX and O&M cost reductions implemented.

Standard Scenarios Model Results

ATB CAPEX, O&M, and capacity factor assumptions for the Base Year and future projections through 2050 for Constant, Mid, and Low technology cost scenarios are used to develop the NREL Standard Scenarios using the ReEDS model. See ATB and Standard Scenarios.

The ReEDS model includes a sensitivity scenario that restricts the resource potential to sites greater than 500 kW, consistent with the Hydropower Vision, which results in 5 GW/29 TWh at 671 dams.

Representative Technology

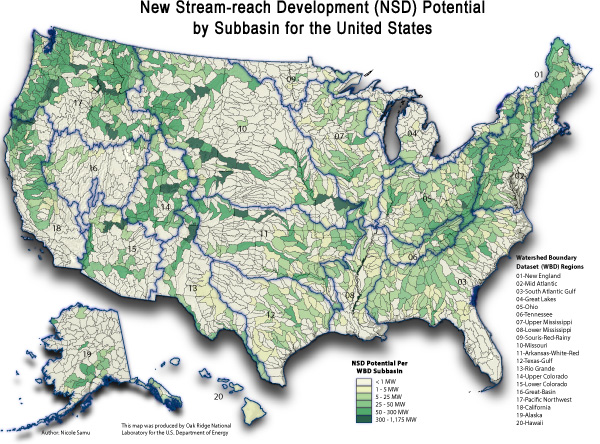

Greenfield or new stream-reach development (NSD) sites are defined as new hydropower developments along previously undeveloped waterways and typically exhibit the following characteristics (DOE, 2016) :

- 1 MW to 100 MW

- New diversion/intake structure

- New penstock

- Steel with length being head/terrain dependent

- Various turbine selections

- Impulse/Francis are common for recently completed projects

- New powerhouse (indoor)

- New tailrace

- New transmission line (up to 15 miles for new projects)

- 30% to 80% capacity factor.

Resource Potential

The resource potential is estimated to be 53.2 GW/301 TWh at nearly 230,000 individual sites (Kao et al., 2014) after accounting for locations statutorily excluded from hydropower development such as national parks, wild and scenic rivers, and wilderness areas.

About 8,500 stream reaches were evaluated to assess resource potential (i.e., capacity) and energy generation potential (i.e., capacity factor). For each stream reach, a design capacity, average monthly flow rate over a 30-year period, and design flow rate exceedance level of 30% are assumed. The exceedance level represents the fraction of time that the design flow is exceeded. This parameter can be varied and results in different capacity and energy generation for a given site. The value of 30% was chosen based on industry rules of thumb. The capacity factor for a given facility is determined by these design criteria. Plant sizes range from kilowatt-scale to multi-megawatt scale (Kao et al., 2014) .

The resource assessment approach is designed to minimize the footprint of a hydropower facility by restricting inundation area to the Federal Emergency Management Agency (FEMA) 100-year floodplain.

New hydropower facilities are assumed to apply run-of-river operation strategies. Run-of-river operation means the flow rate into a reservoir is equal to the flow rate out of the facility. These facilities do not have dispatch capability.

Design capacity and flow rate dictate capacity and energy generation potential. All facilities are assumed sized for 30% exceedance of flow rate based on long-term, average monthly flow rates.

Base Year and Future Year Projections Overview

Site-specific CAPEX, O&M, and capacity factor estimates are made

for each site in the available resource potential. CAPEX and O&M

estimates are made based on statistical analysis of historical plant

data from 1980 to 2015

Projections developed for the Hydropower Vision study (DOE, 2016) using technological learning assumptions and bottom-up analysis of process and/or technology improvements provide a range of future cost outcomes. Three different projections were developed for scenario modeling as bounding levels:

- Constant Technology Cost Scenario: no change in CAPEX, O&M, or capacity factor from 2017 to 2050; consistent across all renewable energy technologies in the ATB

- Mid Technology Cost Scenario: incremental technology learning, consistent with Reference in Hydropower Vision (DOE, 2016); CAPEX reductions for NSD only

- Low Technology Cost Scenario: gains that are achievable

when pushing to the limits of potential new technologies, such as

modularity (in both civil structures and power train design), advanced

manufacturing techniques, and materials, consistent with Advanced

Technology in Hydropower Vision

(DOE, 2016) ; both CAPEX and O&M cost reductions implemented.

Standard Scenarios Model Results

ATB CAPEX, O&M, and capacity factor assumptions for the Base Year and future projections through 2050 for Constant, Mid, and Low technology cost scenarios are used to develop the NREL Standard Scenarios using the ReEDS model. See ATB and Standard Scenarios.

The ReEDS model includes a sensitivity scenario that restricts the resource potential to sites greater than 1 MW, which results in 30.1 GW/176 TWh on nearly 8,000 reaches.

Capital Expenditures (CAPEX): Historical Trends, Current Estimates, and Future Projections

Capital expenditures (CAPEX) are expenditures required to achieve commercial operation in a given year. These expenditures include the hydropower generation plant, the balance of system (e.g., site preparation, installation, and electrical infrastructure), and financial costs (e.g., development costs, onsite electrical equipment, and interest during construction) and are detailed in CAPEX Definition. In the ATB, CAPEX reflects typical plants and does not include differences in regional costs associated with labor, materials, taxes, or system requirements. The related Standard Scenarios product uses regional CAPEX adjustments. The range of CAPEX demonstrates variation with resource in the contiguous United States.

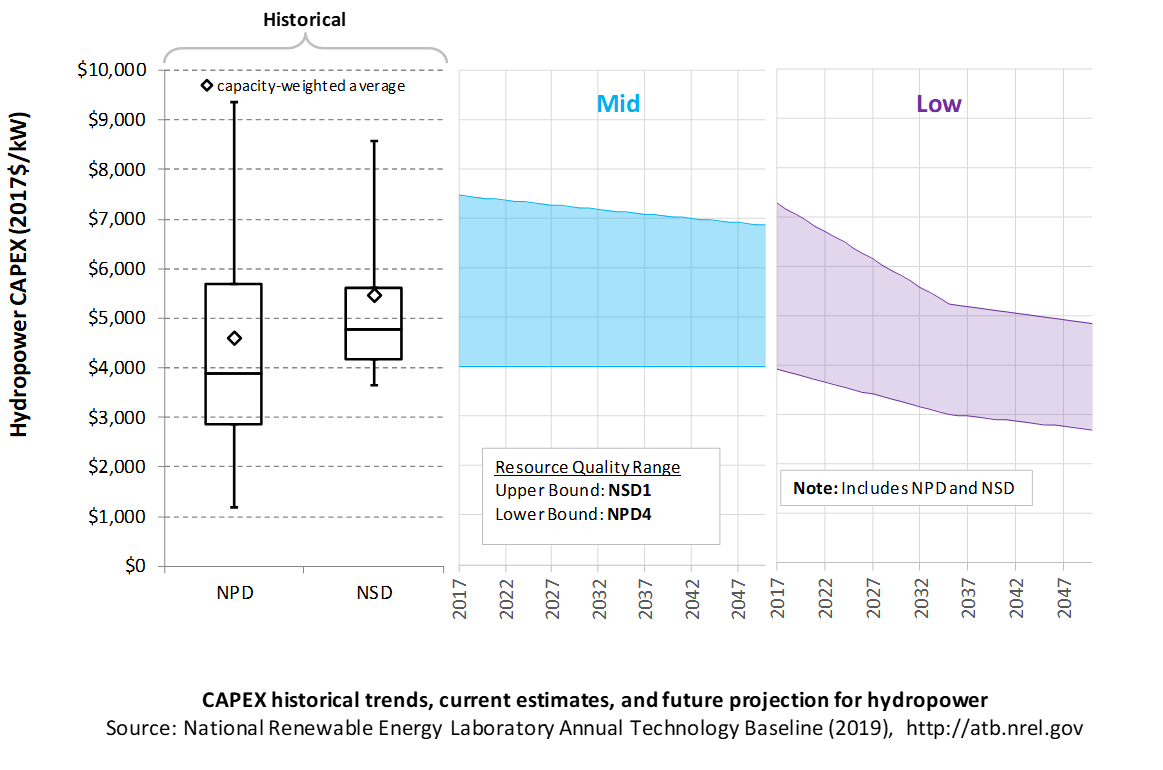

The following figure shows the Base Year estimate and future year projections for CAPEX costs. Mid and Low technology cost scenarios are shown. Historical data from actual and proposed non-powered dam (NPD) and new stream-reach development (NSD) plants installed in the United States from 1981 to 2014 are shown for comparison to the ATB Base Year. The estimate for a given year represents CAPEX of a new plant that reaches commercial operation in that year.

Recent Trends

Actual and proposed NPD and NSD CAPEX from 1981 to 2014

The higher-cost ATB sites generally reflect small-capacity, low head sites that are not comparable to the historical data sample's generally larger-capacity and higher head facilities. These characteristics lead to higher ATB Base Year CAPEX estimates than past data suggest. For example, the NSD projects that became commercially operational in this period are dominated by a few high head projects in the mountains of the Pacific Northwest or Alaska.

The Base Year estimates of CAPEX for NPDs in the ATB range from $3,800/kW to $6,000/kW. These estimates reflect facilities with 3 feet of head to more than 60 feet of head and from 0.5 MW to more than 30 MW of capacity. In general, the higher-cost sites reflect much smaller-capacity (< 10 MW), lower head (< 30 ft.) sites that have fewer analogues in the historical data, but these characteristics result in higher CAPEX.

The Base Year estimates of CAPEX for NSD range from $5,500/kW to $7,900/kW. The estimates reflect potential sites with 3 feet of head to more than 60 feet head and from 1 MW to more than 30 MW of capacity. In general, NSD potential represents smaller-capacity facilities with lower head than most historical data represent. These characteristics lead to higher CAPEX estimates than past data suggest, as many of the larger, higher head sites in the United States have been previously developed.

Base Year Estimates

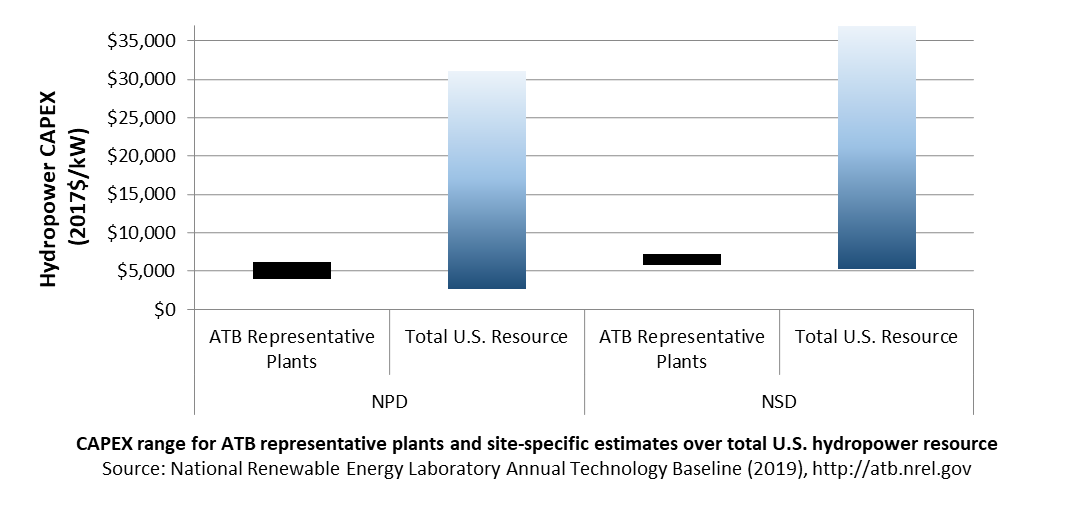

For illustration in the ATB, all potential NPD and NSD sites were first binned by both head and capacity. Analysis of these bins provided groupings that represent the most realistic conditions for future hydropower deployment. The design values of these four reference NPD and four reference NSD plants are shown below. The full range of resource and design characteristics is summarized in the ATB data spreadsheet.

Representative Hydropower Plants

| Resource Characteristics Ranges | Weighted Average Values | Calculated Plant Values | |||||

| Plants | Head (feet) | Capacity (MW) | Head (feet) | Capacity (MW) | Capacity Factor | ICC (2014$/kW) | O&M (2014$/kW) |

| NPD 1 | 3-30 | 0.5-10 | 15.4 | 4.8 | 0.62 | 5,969.33 | 111.73 |

| NPD 2 | 3-30 | 10+ | 15.9 | 82.2 | 0.64 | 5,433.24 | 30.74 |

| NPD 3 | 30+ | 0.5-10 | 89.6 | 4.2 | 0.60 | 3,997.79 | 118.67 |

| NPD 4 | 30+ | 10+ | 81.3 | 44.7 | 0.60 | 3,769.22 | 40.54 |

| NSD 1 | 3-30 | 1-10 | 15.7 | 3.7 | 0.66 | 7,034.81 | 125.01 |

| NSD 2 | 3-30 | 10+ | 19.6 | 44.1 | 0.66 | 6,280.15 | 40.76 |

| NSD 3 | 30+ | 1-10 | 46.8 | 4.3 | 0.62 | 6,151.05 | 117.61 |

| NSD 4 | 30+ | 10+ | 45.3 | 94.0 | 0.66 | 5,537.34 | 28.93 |

The reference plants shown above were developed using the average characteristics (weighted by capacity) of the resource plants within each set of ranges. For example, NPD 1 is constructed from the capacity-weighted average values of NPD sites with 3-30 feet of head and 0.5-10 MW of capacity.

The weighted-average values were used as input to the cost formulas

CAPEX for each plant is based on statistical analysis of historical

plant data from 1980 to 2015 as a function of key design parameters,

plant capacity, and hydraulic head

and

Where P is capacity in megawatts, and H is head in feet. The first term represents the initial capital costs, while the second represents licensing.

Future Projections

Projections developed for the Hydropower Vision study (DOE, 2016) using technological learning assumptions and bottom-up analysis of process and/or technology improvements provide a range of future cost outcomes. Three different CAPEX projections were developed for scenario modeling as bounding levels:

- Constant Technology Cost Scenario:

- NPD and NSD CAPEX unchanged from the Base Year; consistent across all renewable energy technologies in the ATB

- Mid Technology Cost Scenario: consistent with the Reference case in Hydropower Vision:

- NSD CAPEX reduced 5% in 2035 and 8.6% in 2050

- NPD CAPEX unchanged from the Base Year

- Low Technology Cost Scenario: consistent with the Advanced Technology case in Hydropower Vision:

- Low head NPD/All NSD CAPEX reduced 30% in 2035 and 35.3% in 2050. Low Head NPD is NPD-1 and NPD-2

- High head NPD CAPEX reduced 25% in 2035 and 32.7% in 2050; High Head NPD is NPD-3 and NPD-4

A detailed description of the methodology for developing future year projections is found in Projections Methodology.

Technology innovations that could impact future O&M costs are summarized in LCOE Projections.

Standard Scenarios Model Results

ATB CAPEX, O&M, and capacity factor assumptions for the Base Year and future projections through 2050 for Constant, Mid, and Low technology cost scenarios are used to develop the NREL Standard Scenarios using the ReEDS model. See ATB and Standard Scenarios.

The ReEDS model uses resource/cost supply curves representing estimates at each individual facility (~700 NPD and ~8,000 NSD).

The ReEDS model represents cost and performance for NPD and NSD potential in 5 bins for each of 134 geographic regions, which results in CAPEX ranges of $2,750/kW-$9,000/kW for NPD resource and $5,200/kW-$15,600/kW for NSD.

CAPEX Definition