Annual Technology Baseline 2017

National Renewable Energy Laboratory

Recommended Citation:

NREL (National Renewable Energy Laboratory). 2017. 2017 Annual Technology Baseline. Golden, CO: National Renewable Energy Laboratory. http://atb.nrel.gov/.

Please consult Guidelines for Using ATB Data:

https://atb.nrel.gov/electricity/user-guidance.html

Land-Based Wind Power Plants

Representative Technology

Most land-based wind plants in the United States range in capacity from 50 MW to 100 MW (Wiser and Bolinger 2015). Wind turbines installed in the United States in 2015 were, on average, 2-MW turbines with rotor diameters of 102 m and hub heights of 82 m (Moné et al. 2017).

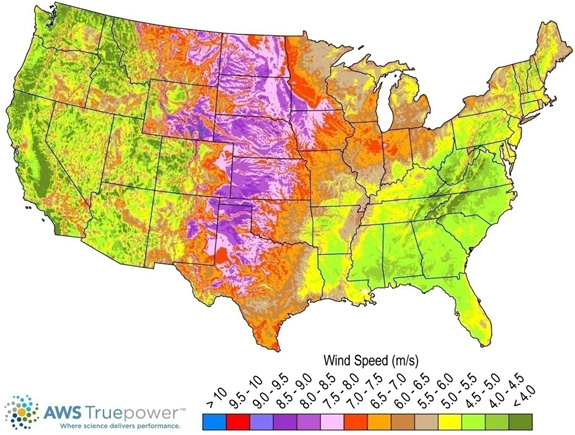

Resource Potential

Wind resource is prevalent throughout the United States but is concentrated in the central states. Total land-based wind technical potential exceeds 10,000 GW (almost tenfold current total U.S. electricity generation capacity), which corresponds to over 3.5 million km2 of potential land area after accounting for standard exclusions such as federally protected areas, urban areas, and water. Resource potential has been expanded from approximately 6,000 GW (DOE 2015) by including locations with lower wind speeds to provide more comprehensive coverage of U.S. land areas where future technology may improve economic potential.

Renewable energy technical potential, as defined by Lopez et al. (2012), represents the achievable energy generation of a particular technology given system performance, topographic limitations and environmental and land-use constraints. The primary benefit of assessing technical potential is that it establishes an upper-boundary estimate of development potential. It is important to understand that there are multiple types of potential-resource, technical, economic, and market (Lopez et al. 2012; NREL, "Renewable Energy Technical Potential").

The resource potential is calculated by using over 130,000 distinct areas for wind plant deployment that cover over 3.5 million km2. The potential capacity is estimated to total over 10,000 GW if a packing density of 3MW/km2 is assumed.

Base Year and Future Year Projections Overview

For each of the 130,000 distinct areas, an LCOE is estimated taking into consideration site-specific hourly wind profiles. Five different wind turbines are associated with a range of average annual wind speed based on actual wind plant installations in 2015. This method is described in Moné et al, (2017) and summarized below.

- The capital expenditures (CAPEX) associated with wind plants installed in 2015 in the interior of the country are used to represent wind plants associated with average annual wind speeds that correspond with the median wind speed for projects installed in 2015. A range of CAPEX across the range of wind speeds is developed using engineering models and assumed differences in rotor diameter. Wind turbines at lower wind speed sites have larger rotors and, therefore, higher CAPEX.

- The capacity factor is determined for each unique geographic location using the site-specific hourly wind profile and a power curve that corresponds with the five wind turbines defined to represent the range of wind technology installed in the United States in 2015.

- Average annual operations and maintenance (O&M) costs are assumed equivalent at all geographic locations.

- LCOE is calculated for each area based on the CAPEX and capacity factor estimated for each area.

For illustration in the ATB, the full resource potential, represented by 130,000 areas, was divided into 10 techno-resource groups (TRGs). The capacity-weighted average CAPEX, O&M, and capacity factor for each group is presented in the ATB.

Future year projections are derived from estimated cost reduction potential for land-based wind technologies based on elicitation of over 160 wind industry experts (Wiser et al. 2016). This study produced three different cost reduction pathways, and the median and low estimates for LCOE reduction are used for ATB Mid and ATB Low cost scenarios. Because the overall LCOE reduction was used as the basis for the ATB projections, all three cost elements - CAPEX, O&M, and capacity factor - should be considered together. The individual component projections are illustrative. Three different projections were developed for scenario modeling as bounding levels:

- High cost: no change in CAPEX, O&M, or capacity factor from 2015 to 2050; consistent across all renewable energy technologies in the ATB

- Mid cost: LCOE percent reduction from the Base Year equivalent to that corresponding to the Median Scenario (50% probability) in expert survey (Wiser et al. 2016)

- Low Cost: LCOE percent reduction from the Base Year equivalent to that corresponding to the Low Scenario (10% probability) in expert survey (Wiser et al. 2016).

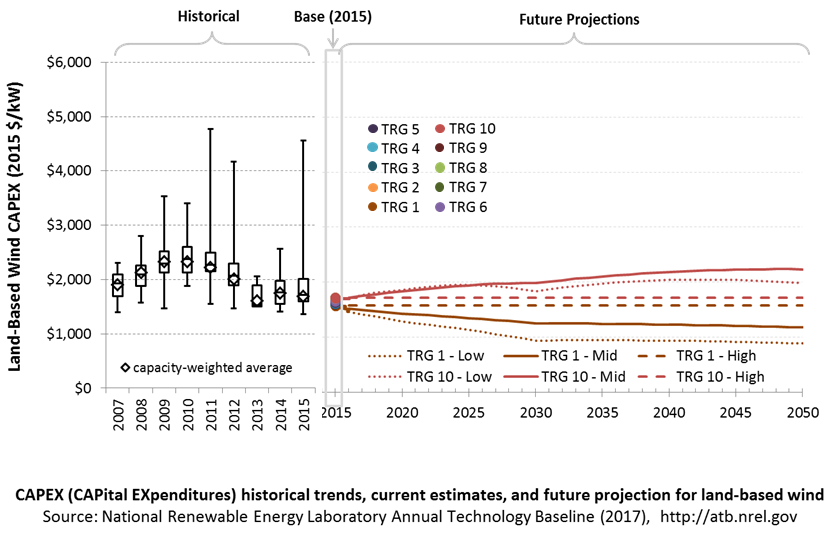

CAPital EXpenditures (CAPEX): Historical Trends, Current Estimates, and Future Projections

Capital expenditures (CAPEX) are expenditures required to achieve commercial operation in a given year. These expenditures include the wind turbine, the balance of system (e.g., site preparation, installation, and electrical infrastructure), and financial costs (e.g., development costs, onsite electrical equipment, and interest during construction) and are detailed in CAPEX Definition. In the ATB, CAPEX reflects typical plants and does not include differences in regional costs associated with labor or materials. The range of CAPEX demonstrates variation with wind resource in the contiguous United States.

The following figure shows the Base Year estimate and future year projections for CAPEX costs. Three cost reduction scenarios are represented: High, Mid, and Low. Historical data from land-based wind plants installed in the United States are shown for comparison to the ATB Base Year estimates. The estimate for a given year represents CAPEX of a new plant that reaches commercial operation in that year.

CAPEX estimates for 2015 correspond well with market data for plants installed in 2015. Projections reflect a continuation of the downward trend observed in the recent past and are anticipated to continue based on preliminary data for 2016 projects.

In the lower wind resource areas represented by TRGs 6-10, CAPEX is likely to grow as future wind turbine technology transitions to new platforms, including taller towers, larger rotors, and higher machine ratings. In the higher wind resource areas represented by TRGs 1-5, optimization of current wind turbine platforms will lead to lower CAPEX in future years.

Recent Trends

Actual land-based wind plant CAPEX (Wiser et al. 2014) is shown in box-and-whiskers format for comparison to the ATB current CAPEX estimates and future projections. Wiser and Bolinger (2014) provide statistical representation of CAPEX for about 65% of wind plants installed in the United States since 2007.

CAPEX estimates should tend toward the low end of observed cost because no regional impacts or spur line costs are included. These effects are represented in the market data.

Base Year Estimates

For illustration in the ATB, all potential land-based wind plant areas were represented in 10 TRGs. These were defined by resource potential (GW) and with higher resolution on the highest-quality TRGs, as these are the most likely sites to be deployed, based on their economics.

TRG 1 represents the best 100 GW of wind, as determined by LCOE. TRG 2 represents the next best 200 GW, while TRG 3 represents the next best 400 GW, and TRG 4 represents the next best 800 GW. TRGs 5-9 all represent 1,600 GW of resource potential. TRG 10 represents the remaining 1,148 GW of available potential. This representation is based on the approach described in DOE (2015) and implemented with 2015 market data in Moné et al. (2017).

The table below summarizes the annual average wind speed range for each TRG, capacity-weighted average wind speed, cost and performance parameters for each TRG, and resource potential in terms of capacity and energy for each TRG. Typical land-based wind installations in 2015 are associated with TRG 4.

| Techno-Resource Group (TRG) | Wind Speed Range (m/s) | Weighted Average Wind Speed (m/s) | Weighted Average CAPEX ($/kW) | Weighted Average OPEX ($/kW/yr) | Weighted Average Net CF (%) | Potential Wind Plant Capacity (GW) | Potential Wind Plant Energy (TWh) |

|---|---|---|---|---|---|---|---|

| TRG1 | 8.2–13.5 | 8.7 | 1,573 | 51 | 47.4% | 100 | 414 |

| TRG2 | 8.0–10.9 | 8.4 | 1,592 | 51 | 46.2% | 200 | 810 |

| TRG3 | 7.7–11.1 | 8.2 | 1,599 | 51 | 45.0% | 400 | 1,576 |

| TRG4 | 7.5–13.1 | 7.9 | 1,605 | 51 | 43.5% | 800 | 3,050 |

| TRG5 | 6.9–11.1 | 7.5 | 1,616 | 51 | 40.7% | 1,600 | 5,708 |

| TRG6 | 6.1–9.4 | 6.9 | 1,642 | 51 | 36.4% | 1,600 | 5,098 |

| TRG7 | 5.4–8.3 | 6.2 | 1,678 | 51 | 30.8% | 1,600 | 4,320 |

| TRG8 | 4.7–6.9 | 5.5 | 1,708 | 51 | 24.6% | 1,600 | 3,443 |

| TRG9 | 4.0–6.0 | 4.8 | 1,713 | 51 | 18.3% | 1,600 | 2,558 |

| TRG10 | 1.0–5.3 | 4.0 | 1,713 | 51 | 11.1% | 1,148 | 1,116 |

| Total | 10,648 | 28,092 | |||||

Future Year Projections

Projections of future LCOE were derived from a survey of wind industry experts (Wiser et al. 2016) for scenarios that are associated with 50% and 10% probability levels in 2030 and 2050. Projections of future offshore wind plant CAPEX was determined based on adjustments to CAPEX, fixed O&M (FOM), and capacity factor in each year to result in a predetermined LCOE value based on an expert survey conducted by Wiser et al. (2016).

In order to achieve the overall LCOE reduction associated with the median and low projections from the expert survey, CAPEX was used to accommodate all improvement aspects other than O&M and capacity factor survey results. In the lower wind resource areas represented by TRGs 6-10, CAPEX is likely to grow as future wind turbine technology transitions to new platforms, including taller towers, larger rotors, and higher machine ratings. In the higher wind resource areas represented by TRGs 1-5, optimization of current wind turbine platforms will lead to lower CAPEX.

A detailed description of the methodology for developing future year projections is found in Projections Methodology.

Technology innovations that could impact future CAPEX costs are summarized in LCOE Projections.

CAPEX Definition

Capital expenditures (CAPEX) are expenditures required to achieve commercial operation in a given year.

For the ATB - and based on EIA (2016a) and the System Cost Breakdown Structure defined by Moné et al. (2015) - the wind plant envelope is defined to include:

- Wind turbine supply

- Balance of system (BOS)

- Turbine installation, substructure supply, and installation

- Site preparation, installation of underground utilities, access roads, and buildings for operations and maintenance

- Electrical infrastructure, such as transformers, switchgear, and electrical system connecting turbines to each other and to the control center

- Project-related indirect costs, including engineering, distributable labor and materials, construction management start up and commissioning, and contractor overhead costs, fees, and profit.

- Financial costs

- Owner's costs, such as development costs, preliminary feasibility and engineering studies, environmental studies and permitting, legal fees, insurance costs, and property taxes during construction

- Onsite electrical equipment (e.g., switchyard), a nominal-distance spur line (^lt;1 mile), and necessary upgrades at a transmission substation; distance-based spur line cost (GCC) not included in the ATB

- Interest during construction estimated based on three-year duration accumulated 10%/10%/80% at half-year intervals and an 8% interest rate (ConFinFactor).

CAPEX can be determined for a plant in a specific geographic location as follows:

CAPEX = ConFinFactor*(OCC*CapRegMult+GCC).

(See the Financial Definitions tab in the ATB data spreadsheet.)

Regional cost variations and geographically specific grid connection costs are not included in the ATB (CapRegMult = 1; GCC = 0). In the ATB, the input value is overnight capital cost (OCC) and details to calculate interest during construction (ConFinFactor).

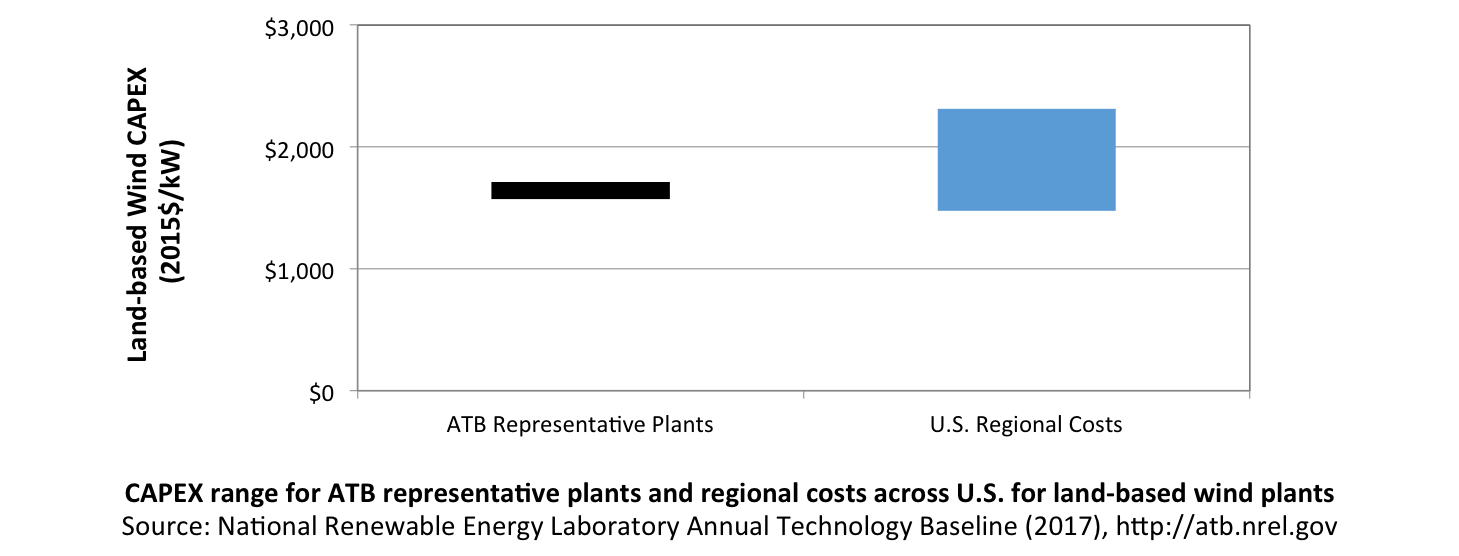

In the ATB, CAPEX represents a typical land-based wind plant and varies with annual average wind speed. Regional cost effects associated with labor rates, material costs, and other regional effects as defined by EIA (2016a), DOE (2015) expand the range of CAPEX. Unique land-based spur line costs for each of the 130,000 areas based on distance and transmission line costs expand the range of CAPEX even further. The figure below illustrates the ATB representative plants relative to the range of CAPEX including regional costs across the contiguous United States. Note that the ATB Base Year estimate for TRG 4 is equivalent to the market data observed capacity-weighted average wind plant CAPEX in the same year. The ATB representative plants are associated with a regional multiplier of 1.0.

Standard Scenarios Model Results

ATB CAPEX, O&M, and capacity factor assumptions for Base Year and future projections through 2050 for High, Mid, and Low projections are used to develop the NREL Standard Scenarios using the ReEDS model. See ATB and ATB and Standard Scenarios.

CAPEX in the ATB does not represent regional variants (CapRegMult) associated with labor rates, material costs, etc., but the ReEDS model does include 134 regional multipliers (EIA 2016a).

The ReEDS model determines the land-based spur line (GCC) uniquely for each of the 130,000 areas based on distance and transmission line cost.

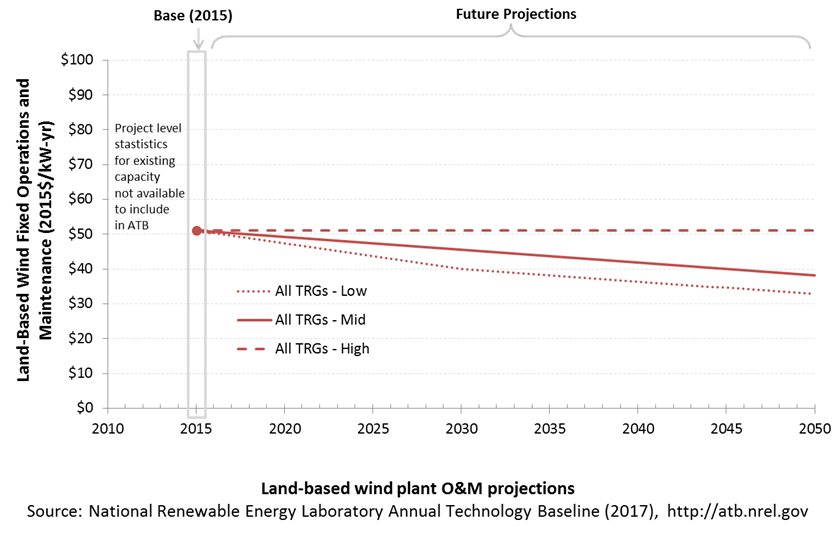

Operation and Maintenance (O&M) Costs

Operations and maintenance (O&M) costs represent the annual fixed expenditures (and depend on capacity) required to operate and maintain a wind plant over its technical lifetime of 25 years (the distinction between economic life and technical life is described here), including:

- Insurance, taxes, land lease payments, and other fixed costs

- Present value, annualized large component costs over technical life (e.g., blades, gearboxes, generators)

- Scheduled and unscheduled maintenance of wind plant components including turbines, transformers, etc. over the technical lifetime of the plant.

The following figure shows the Base Year estimate and future year projections for fixed O&M (FOM) costs. Three cost reduction scenarios are represented. The estimate for a given year represents annual average FOM costs expected over the technical lifetime of a new plant that reaches commercial operation in that year.

Base Year Estimates

Due to a lack of robust market data, an assumption of FOM of $51/kW-yr was determined to be representative of the range of available data; no variation of FOM with TRG (or wind speed) was assumed (DOE 2015).

Future Year Projections

Future FOM is assumed to decline 25% by 2050 in Mid cost case and 39% in Low cost wind cases. These values are the result of linear curves fit to the results of the expert survey documented in Wiser et al. (2016).

A detailed description of the methodology for developing future year projections is found in Projections Methodology. A detailed description of the methodology for developing future year projections is found in Projections Methodology.

Technology innovations that could impact future O&M costs are summarized in LCOE Projections.

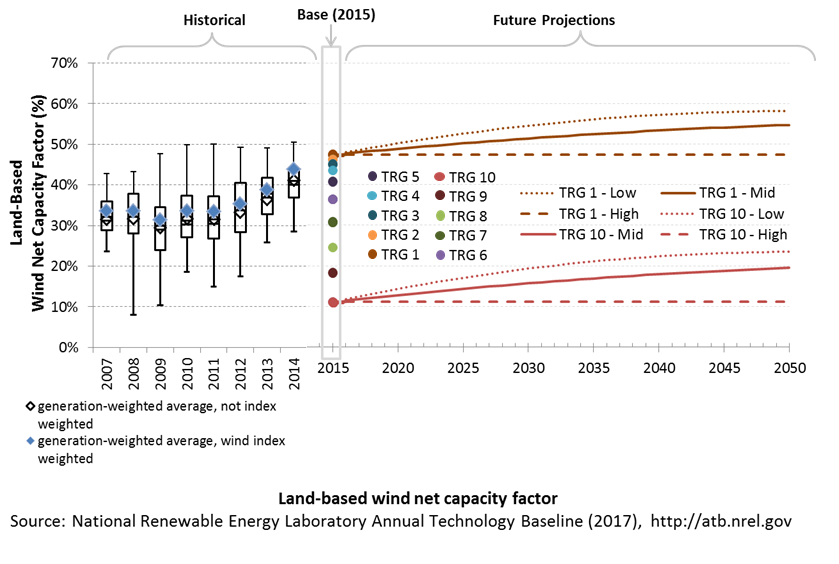

Capacity Factor: Expected Annual Average Energy Production Over Lifetime

The capacity factor represents the expected annual average energy production divided by the annual energy production, assuming the plant operates at rated capacity for every hour of the year. It is intended to represent a long-term average over the technical lifetime of the plant (the distinction between economic life and technical life is described here). It does not represent interannual variation in energy production. Future year estimates represent the estimated annual average capacity factor over the technical lifetime of a new plant installed in a given year.

The capacity factor is influenced by hourly wind profile, expected downtime, and energy losses within the wind plant. The specific power (ratio of machine rating to rotor swept area) and hub height are design choices that influence the capacity factor.

The following figure shows a range of capacity factors based on variation in the resource for wind plants in the contiguous United States. Historical data from wind plants operating in the United States in 2015, according to the year in which plants were installed, is shown for comparison to the ATB Base Year estimates. The range of Base Year estimates illustrate the effect of locating a wind plant in sites with high wind speeds (TRG 1) or low wind speeds (TRG 10). Future projections are shown for High, Mid, and Low cost scenarios.

Recent Trends

Actual energy production from about 90% of wind plants operating in the United States since 2007 (Wiser et al. 2014) is shown in box-and-whiskers format for comparison with the ATB current estimates and future projections. The historical data illustrate capacity factor for projects operating in 2015, shown by year of commercial online date. As reported in the 2015 DOE Wind Technologies Market Report (Wiser and Bolinger 2016), NextEra Energy Resources, in their quarterly earnings reports, estimates that the "wind resource index" for the United States as a whole was 94% in 2015. The generation-weighted average 2015 capacity factors are also shown adjusted upward for a typical wind resource year by 1/0.94.

Base Year Estimates

For illustration in the ATB, all potential land-based wind plant areas were represented in 10 TRGs. The capacity-weighted average CAPEX, capacity factor, and resource potential are shown in the table below.

| Techno-Resource Group (TRG) | Wind Speed Range (m/s) | Weighted Average Wind Speed (m/s) | Weighted Average CAPEX ($/kW) | Weighted Average OPEX ($/kW/yr) | Weighted Average Net CF (%) | Potential Wind Plant Capacity (GW) | Potential Wind Plant Energy (TWh) |

|---|---|---|---|---|---|---|---|

| TRG1 | 8.2–13.5 | 8.7 | 1,573 | 51 | 47.4% | 100 | 414 |

| TRG2 | 8.0–10.9 | 8.4 | 1,592 | 51 | 46.2% | 200 | 810 |

| TRG3 | 7.7–11.1 | 8.2 | 1,599 | 51 | 45.0% | 400 | 1,576 |

| TRG4 | 7.5–13.1 | 7.9 | 1,605 | 51 | 43.5% | 800 | 3,050 |

| TRG5 | 6.9–11.1 | 7.5 | 1,616 | 51 | 40.7% | 1,600 | 5,708 |

| TRG6 | 6.1–9.4 | 6.9 | 1,642 | 51 | 36.4% | 1,600 | 5,098 |

| TRG7 | 5.4–8.3 | 6.2 | 1,678 | 51 | 30.8% | 1,600 | 4,320 |

| TRG8 | 4.7–6.9 | 5.5 | 1,708 | 51 | 24.6% | 1,600 | 3,443 |

| TRG9 | 4.0–6.0 | 4.8 | 1,713 | 51 | 18.3% | 1,600 | 2,558 |

| TRG10 | 1.0–5.3 | 4.0 | 1,713 | 51 | 11.1% | 1,148 | 1,116 |

| Total | 10,648 | 28,092 | |||||

The majority of installed U.S. wind plants generally align with ATB estimates for performance in TRGs 5-7. High wind resource sites associated with TRGs 1 and 2 as well as very low wind resource sites associated with TRGs 8-10 are not as common in the historical data, but the range of observed data encompasses ATB estimates.

The capacity factor is referenced to an 80-m, above-ground-level, long-term average hourly wind resource data from AWS Truepower (2012).

Future Year Projections

Projections for capacity factors implicitly reflect technology innovations such as larger rotors and taller towers that will increase energy capture at the same location without specifying precise tower height or rotor diameter changes. Projections of capacity factor for plants installed in future years were determined based on adjustments to CAPEX, FOM, and capacity factor in each year to result in a predetermined LCOE value.

A detailed description of the methodology for developing future year projections is found in Projections Methodology.

Technology innovations that could impact future capacity factors are summarized in LCOE Projections.

Standard Scenarios Model Results

ATB CAPEX, O&M, and capacity factor assumptions for Base Year and future projections through 2050 for High, Mid, and Low projections are used to develop the NREL Standard Scenarios using the ReEDS model. See ATB and Standard Scenarios.

The ReEDS model output capacity factors for wind and solar PV can be lower than input capacity factors due to endogenously estimated curtailments determined by scenario constraints.

Plant Cost and Performance Projections Methodology

ATB projections were derived from the results of a survey of 163 of the world's wind energy experts (Wiser et al. 2016). The survey was conducted to gain insight into the possible future cost reductions, the source of those reductions, and the conditions needed to enable continued innovation and lower costs (Wiser et al. 2016). The expert survey produced three cost reduction scenarios associated with probability levels of 10%, 50%, and 90% of achieving LCOE reductions by 2030 and 2050. In addition, the scenario results include estimated changes to CAPEX, O&M, capacity factor, project life, and weighted average cost of capital (WACC) by 2030.

For the ATB, three different projections were adapted from the expert survey results for scenario modeling as bounding levels:

- High Cost: no change in CAPEX, O&M, or capacity factor from 2015 to 2050, consistent across all renewable energy technologies in ATB.

- Mid cost: LCOE percent reduction from the Base Year equivalent to that corresponding to the Median Scenario (50% probability) in the expert survey (Wiser et al. 2016)

- Low cost: LCOE percent reduction from the Base Year equivalent to that corresponding to the Low scenario (10% probability) in the expert survey (Wiser et al. 2016).

Expert survey estimates were normalized to the ATB Base Year starting point in order to focus on projected cost reduction instead of absolute reported costs. The percent reductions in LCOE by 2020, 2030, and 2050 from the expert survey's Median and Low scenarios are implemented as the ATB Mid and Low cost scenarios. This is accomplished by utilizing survey estimates for changes to capacity factor and O&M costs by 2030 and 2050. The corresponding CAPEX value to achieve the overall LCOE reduction is computed. The percent reduction in LCOE by 2030 and by 2050 was applied equally across all TRGs. The overall reduction in LCOE by 2050 for the Mid cost scenario is 35% and for the Low cost scenario is 53%.

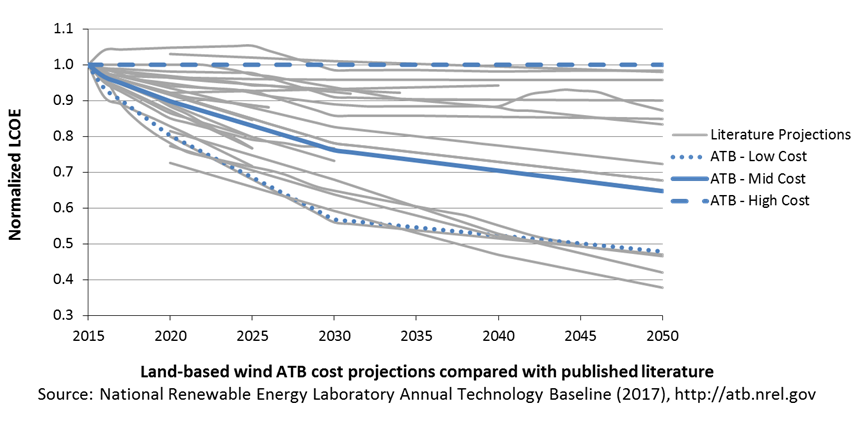

A broad sample of cost of wind energy projections are shown to provide context for the ATB High, Mid, and Low cost projections. The ATB Mid cost projection, which corresponds to the Median scenario from the expert survey, results in LCOE reductions that are lower than median scenarios in the literature. The ATB Low cost projection, which corresponds to the Low scenario from the expert survey, is similar to the lower bound of the sample of literature projections.

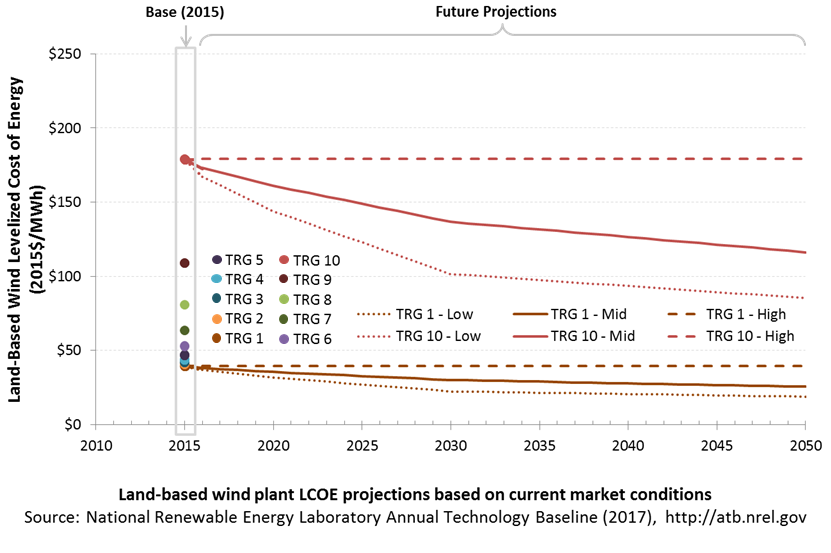

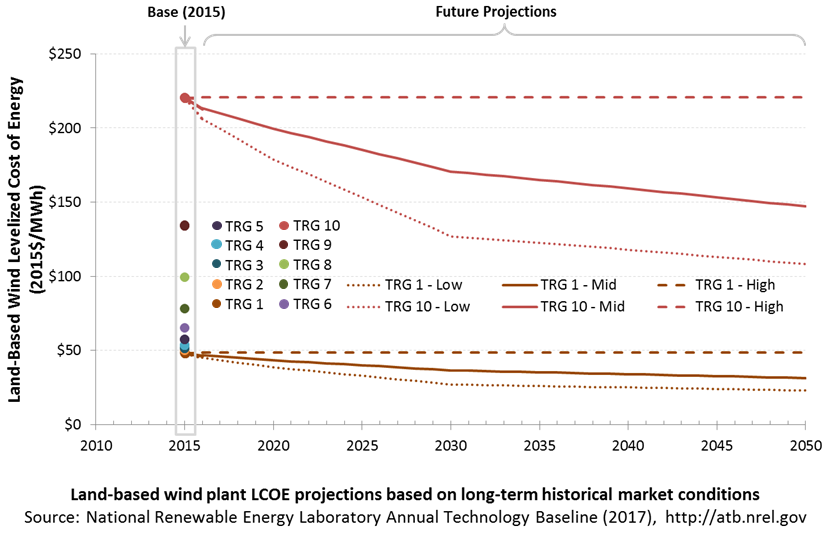

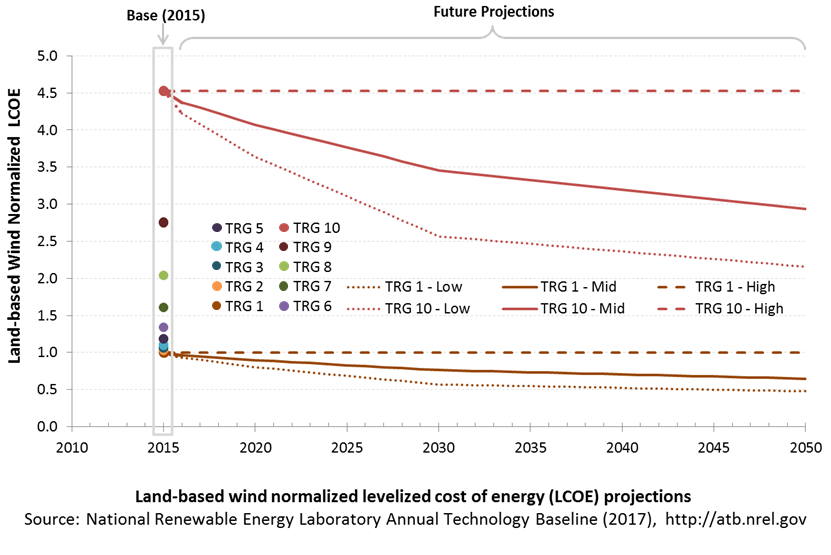

Levelized Cost of Energy (LCOE) Projections

Levelized cost of energy (LCOE) is a simple metric that combines the primary technology cost and performance parameters, CAPEX, O&M, and capacity factor. It is included in the ATB for illustrative purposes. The focus of the ATB is to define the primary cost and performance parameters for use in electric sector modeling or other analysis where more sophisticated comparisons among technologies are made. LCOE captures the energy component of electric system planning and operation, but the electric system also requires capacity and flexibility services to operate reliably. Electricity generation technologies have different capabilities to provide such services. For example, wind and PV are primarily energy service providers, while the other electricity generation technologies provide capacity and flexibility services in addition to energy. These capacity and flexibility services are difficult to value and depend strongly on the system in which a new generation plant is introduced. These services are represented in electric sector models such as the ReEDS model and corresponding analysis results such as the Standard Scenarios.

The following three figures illustrate the combined impact of CAPEX, O&M, and capacity factor projections across the range of resources present in the contiguous United States. The Current Market Conditions LCOE demonstrates the range of LCOE based on macroeconomic conditions similar to the present. The Historical Market Conditions LCOE presents the range of LCOE based on macroeconomic conditions consistent with prior ATB editions and Standard Scenarios model results. The Normalized LCOE (all LCOE estimates are normalized with the lowest Base Year LCOE value) emphasizes the effect of resource quality and the relative differences in the three future pathways independent of project finance assumptions. The ATB representative plant characteristics that best align with recently installed or anticipated near-term land-based wind plants are associated with TRG 4. Data for all the resource categories can be found in the ATB data spreadsheet.

The methodology for representing the CAPEX, O&M, and capacity factor assumptions behind each pathway is discussed in Projections Methodology. The three pathways are generally defined as:

- High = Base Year (or near-term estimates of projects under construction) equivalent through 2050 maintains current relative technology cost differences

- Mid = technology advances through continued industry growth, public and private R&D investments, and market conditions relative to current levels that may be characterized as "likely" or "not surprising"

- Low = Technology advances that may occur with breakthroughs, increased public and private R&D investments, and/or other market conditions that lead to cost and performance levels that may be characterized as the "limit of surprise" but not necessarily the absolute low bound.

To estimate LCOE, assumptions about the cost of capital to finance electricity generation projects are required. For comparison in the ATB, two project finance structures are represented.

- Current Market Conditions: The values of the production tax credit (PTC) and investment tax credit (ITC) are ramping down by 2020, at which time wind and solar projects may be financed with debt fractions similar to other technologies. This scenario reflects debt interest (4.4% nominal, 1.9% real) and return on equity rates (9.5% nominal, 6.8% real) to represent 2017 market conditions (AEO 2017) and a debt fraction of 60% for all electricity generation technologies. An economic life, or period over which the initial capital investment is recovered, of 20 years is assumed for all technologies. These assumptions are one of the project finance options in the ATB spreadsheet.

- Long-Term Historical Market Conditions: Historically, debt interest and return on equity were represented with higher values. This scenario reflects debt interest (8% nominal, 5.4% real) and return on equity rates (13% nominal, 10.2% real) implemented in the ReEDS model and reflected in prior versions of the ATB and Standard Scenarios model results. A debt fraction of 60% for all electricity generation technologies is assumed. An economic life, or period over which the initial capital investment is recovered, of 20 years is assumed for all technologies. These assumptions are one of the project finance options in the ATB spreadsheet.

These parameters are held constant for estimates representing the Base Year through 2050. No incentives such as the PTC or ITC are included. The equations and variables used to estimate LCOE are defined on the equations and variables page. For illustration of the impact of changing financial structures such as WACC and economic life, see Project Finance Impact on LCOE. For LCOE estimates for High, Mid, and Low scenarios for all technologies, see 2017 ATB Cost and Performance Summary.

In general, the degree of adoption of a range of technology innovations distinguishes the High, Mid and Low cost cases. These projections represent the following trends to reduce CAPEX and FOM, and increase O&M.

- Continued turbine scaling to larger-megawatt turbines with larger rotors such that the swept area/megawatt capacity decreases, resulting in higher capacity factors for a given location

- Continued diversity of turbine technology whereby the largest rotor diameter turbines tend to be located in lower wind speed sites, but the number of turbine options for higher wind speed sites increases

- Taller towers that result in higher capacity factors for a given site due to the wind speed increase with elevation above ground level

- Improved plant siting and operation to reduce plant-level energy losses, resulting in higher capacity factors

- More efficient O&M procedures combined with more reliable components to reduce annual average FOM costs

- Continued manufacturing and design efficiencies such that capital cost/kilowatt decreases with larger turbine components

- Adoption of a wide range of innovative control, design, and material concepts that facilitate the above high-level trends.

References

AWS Truepower. 2012. Wind Resource of the United States: Mean Annual Wind Speed at 200m Resolution. https://www.awstruepower.com/assets/Wind-Resource-Map-UNITED-STATES-11x171.pdf.

DOE (U.S. Department of Energy). 2015. Wind Vision: A New Era for Wind Power in the United States. U.S. Department of Energy. DOE/GO-102015-4557. March 2015. http://energy.gov/sites/prod/files/2015/03/f20/wv_full_report.pdf.

EIA (U.S. Energy Information Administration). 2016a. Capital Cost Estimates for Utility Scale Electricity Generating Plants. Washington, D.C.: U.S. Department of Energy. November 2016. https://www.eia.gov/analysis/studies/powerplants/capitalcost/pdf/capcost_assumption.pdf.

EIA (U.S. Energy Information Administration). 2017. Annual Energy Outlook 2017 with Projections to 2050. Washington, D.C.: U.S. Department of Energy. January 5, 2017. http://www.eia.gov/outlooks/aeo/pdf/0383(2017).pdf.

Lopez, Anthony, Billy Roberts, Donna Heimiller, Nate Blair, and Gian Porro. 2012. U.S. Renewable Energy Technical Potentials: A GIS-Based Analysis. National Renewable Energy Laboratory. NREL/TP-6A20-51946. http://www.nrel.gov/docs/fy12osti/51946.pdf.

Moné, C., A. Smith, M. Hand, and B. Maples. 2015. 2013 Cost of Wind Energy Review. Golden, CO: National Renewable Energy Laboratory. http://www.nrel.gov/docs/fy15osti/63267.pdf.

Moné, Christopher, Maureen Hand, Mark Bolinger, Joseph Rand, Donna Heimiller, and Jonathan Ho. 2017. 2015 Cost of Wind Energy Review. Golden, CO: National Renewable Energy Laboratory. NREL/TP-6A20-66861. http://www.nrel.gov/docs/fy17osti/66861.pdf.

Wiser, Ryan, and Mark Bolinger. 2016. 2015 Wind Technologies Market Report. August 2016. https://emp.lbl.gov/sites/default/files/2015-windtechreport.final_.pdf.

Wiser, Ryan, Karen Jenni, Joachim Seel, Erin Baker, Maureen Hand, Eric Lantz, and Aaron Smith. 2016. Forecasting Wind Energy Costs and Cost Drivers: The Views of the World's Leading Experts. Berkeley, CA: Lawrence Berkeley National Laboratory. LBNL-1005717. June 2016. https://emp.lbl.gov/publications/forecasting-wind-energy-costs-and.

Wiser, Ryan, Mark Bolinger, Galen Barbose, Naïm Darghouth, Ben Hoen, Andrew Mills, Samantha Weaver, Kevin Porter, Michael Buckley, Frank Oteri, and Suzanne Tegen. 2014. 2013 Wind Technologies Market Report. Washington, D.C.: U.S. Department of Energy. DOE/GO-102014-4459. August 2014. https://energy.gov/sites/prod/files/2014/08/f18/2013%20Wind%20Technologies%20Market%20Report_1.pdf.